Then please join us for a one-hour seminar on Wednesday, August 12 at 6:30pm that will cover key information you need to know.

We’re excited to be bringing together experts like Stephanie Viva, Executive Director of the Mashpee Chamber of Commerce, who will talk about the Cape’s economic outlook for the fall; Patti Lotane, Cape Cod 5 senior mortgage banker, who will describe some of the various financing options your buyers may be considering, and Atty. Bryan Reardon, from the firm of Dubin & Reardon, who will outline how the selling process has changed since you last bought your home.

We’ll be talking about current market conditions and how you can best position your property for a successful sale.

The presentations will be brief so there can be plenty of time for questions and talk around the table.

The event is being held at the Cape Space/Mashpee Chamber offices in Mashpee Commons. We’ll have some light bites and beverages for you, too.

Seating is limited, so please let us know at 508-388-1994 or msennott@todayrealestate.com if you will be attending.

It’s n0 secret: Cape Cod home prices sit well above the national average, and that gap has only widened in recent years. The core takeaway is simple: if you’re feeling squeezed by Cape Cod’s market, there are plenty of appealing, more affordable regions across the country where budgets stretch further without sacrificing quality of life.

Cape Cod’s pricing reality

The Cape’s median single‑family home price now hovers around $800,000–$900,000, driven by limited inventory, strong second‑home demand, and our appealing environment. (Remember: median means the price in the middle. There are as many homes for sale below that price as above.)

Homes that are price correctly still can attract multiple offers, and renovation‑ready properties often command premium prices. For many buyers—especially first‑timers—this creates a sense that homeownership is slipping out of reach.

More affordable regions across the U.S.

If Cape Cod feels too steep, several areas of the country offer significantly lower median prices, often $250,000–$400,000, with strong communities, job markets, and lifestyle perks.

Midwest cities — Places like Columbus, Indianapolis, and Kansas City offer stable economies and median prices often under $350,000. Buyers can find newer construction, larger lots, and vibrant neighborhoods without coastal premiums.

Southern metros — Greenville, Knoxville, and Charleston (pictured above) combine affordability with growing job markets. Median prices frequently fall between $275,000–$375,000, and cost‑of‑living advantages amplify purchasing power.

Mountain West towns — While some areas have surged, places like suburban Boise, Billings, or parts of New Mexico still offer attainable pricing and outdoor‑focused lifestyles.

Rust Belt revivals — Buffalo, Cleveland, and Pittsburgh continue to reinvent themselves, offering historic homes, strong cultural scenes, and median prices well below national averages.

Why exploring other markets makes sense

Cape Cod’s charm is undeniable—beaches, community, and coastal character—but its pricing reflects scarcity. In contrast, many inland or emerging markets offer:

More square footage for the dollar

Lower property taxes

Newer construction options

Stronger affordability for first‑time buyers

For anyone feeling discouraged by the Cape’s price tags, expanding your search radius can transform your buying experience. The U.S. housing landscape is incredibly diverse, and affordability varies widely. Exploring other regions doesn’t mean giving up on Cape Cod forever—it simply opens doors to homeownership that may feel closed here.

If you’re interested in exploring options in other parts of the country, we can help. Because of our long-time association with the Tom Ferry Organization — our industry’s largest and most respected training organization — we know agents from across the country. We can connect you with a qualified real estate professional whether you’re interested in Columbus, Knoxville, or Boise.

Just let us know. You can always find us at (508)-388-1994 [Mari and Hank] or (781) 264-5517 [Colleen].

Mari, Hank, and Colleen

PS: We’re not ones to brag, but we’re excited to tell you that we earned Agents of the Month for June at Today RE. We were involved in nine successful transactions last month. It’s said that the average, active Cape Cod realtor has three successful transactions over a year! Many thanks to our clients who trusted us to help them find where’s next. When you love what you do, it’s not work.

If you’ve had moving on your mind during the first half of the year, you may be feeling stuck. (BTW…you’re not the only one.)

Mortgage rates stayed higher than people wanted. Affordability remained tight. And uncertainty overseas added another layer of pressure nobody saw coming.

So the question is: Will the second half of the year be any better for the housing market?

While no one can say for sure, there are a few encouraging signs that the market could start moving in a better direction. Here’s what to watch.

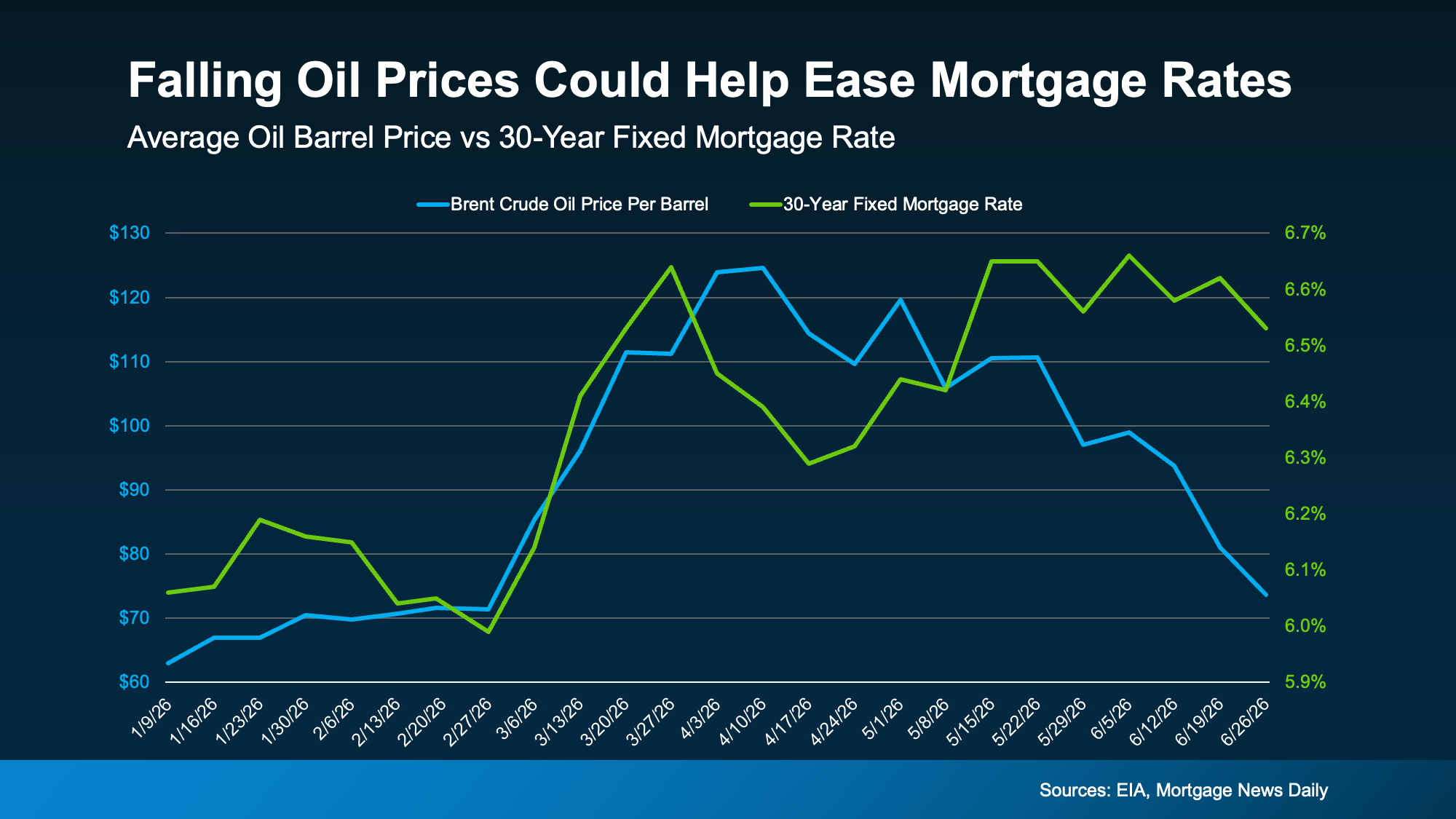

Mortgage Rates Could Be Near a Turning Point

One of the biggest reasons mortgage rates haven’t come down yet is inflation. And higher energy prices and uncertainty overseas are at least part of the reason inflation is still elevated. The encouraging news?

Oil prices seem to be coming back down. What does that have to do with buying a home? It’s because historically, mortgage rates and oil prices tend to move in the same direction.

Take a look at the graph below. Generally, they rise and fall together. Both went up in February when the conflict with Iran began. While there’s still been some volatility, experts at the U.S. Energy Information Administration (EIA) say oil prices are forecast to come down. And since oil prices have been on an overall downward trend lately, mortgage rates could come down too:

It’s too soon to say exactly when that will happen (or by how much they’ll fall), but if energy prices go down, inflation cools off, and tensions overseas ease, mortgage rates could come down in the second half of the year.

And that’s good news for anyone thinking about moving. The first half of the year tested everyone’s patience. The second half may finally reward it.

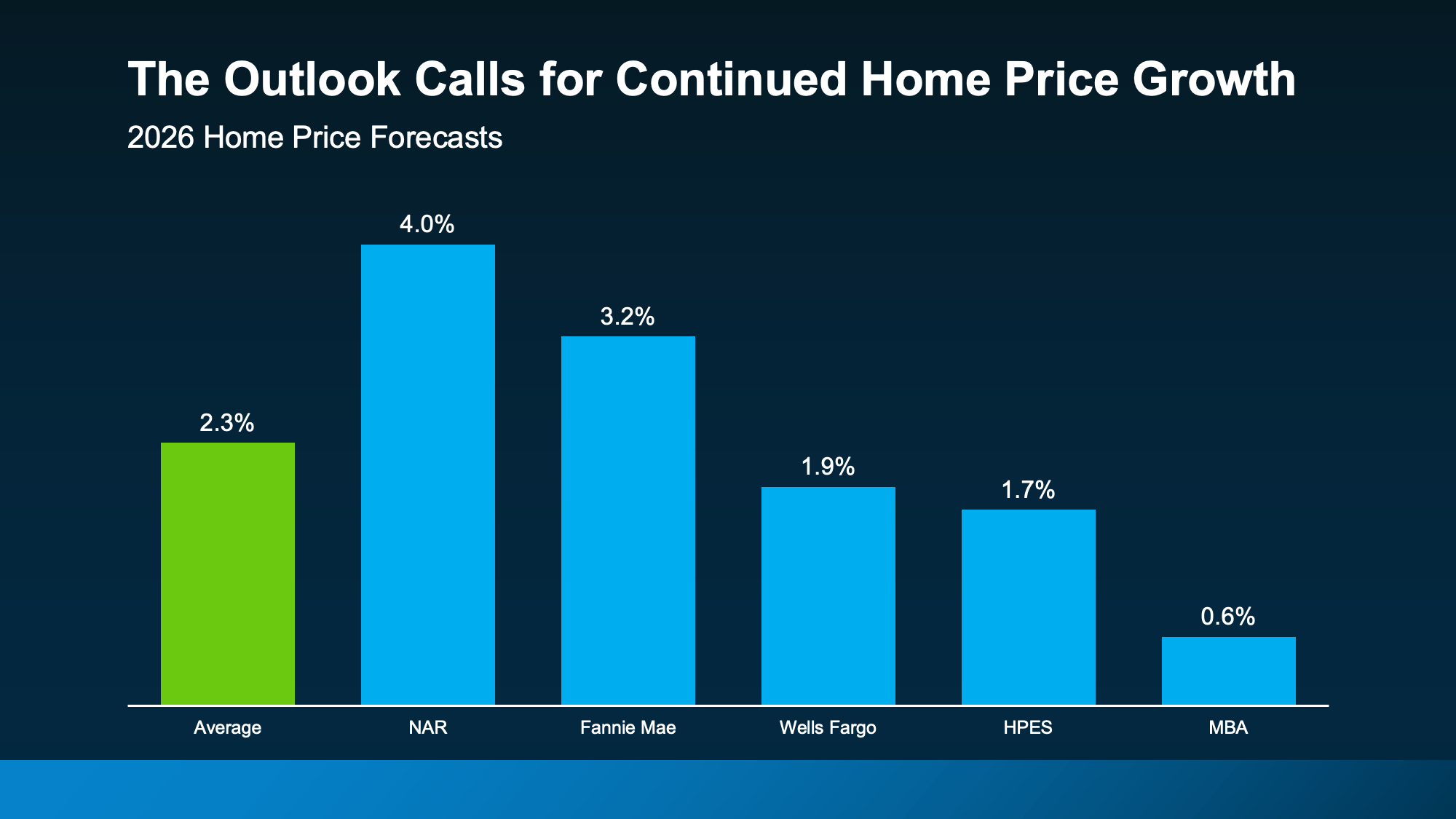

Home Prices Could Pick Back Up

A lot of people want home prices to fall, too. But that’s not what most forecasts show.

While price trends are going to vary by area, and some places are seeing mild declines, experts still expect home prices to net positive this year at the national level.

In fact, they’re projecting prices will rise by an average of 2.3% in 2026 (see graph below):

What does that mean for you? Right now, Federal Housing Finance Agency (FHFA) data shows prices are up about 1.7% nationally year-over-year. The average forecast for all of 2026? 2.3%.

Based on those projections, home price growth would have to pick up a bit during the second half of the year. Nothing dramatic, just enough to finish the year around that projected 2.3% gain.

Here’s why that’s possible.

The number of homes for sale has grown, but that growth may be starting to slow down. And if rates improve, more buyers could jump back into the market. More buyers competing could put modest upward pressure on prices, especially if inventory’s not growing as fast.

That’s why buyers shouldn’t assume waiting will guarantee a lower price later. (It never really does.) For sellers, that’s great news if you’ve been worried about your home’s value.

More Homes Are Expected To Sell

If you’ve been wondering why the housing market has felt quieter lately, you’re not imagining it. Home sales have been slower than many experts expected. But that doesn’t mean people have stopped wanting to move.

In fact, for the first half of the year Today Real Estate has exceeded expectations for successful transactions!

We’ve been able to help our clients close on 15 properties during the first half of the year. It is said that the average, active Cape Cod realtor has three successful transactions over the course of a year!

Bottom Line

A lot of people still want or need to make a change. They’ve just been waiting for more certainty, better affordability, or a clearer read on where the market is headed. And early signs show that may be on the horizon.

Mortgage rates may ease. Home sales could pick up. And prices are expected to continue rising at a healthier, more sustainable pace. If you’ve been waiting for signs of progress, this is it.

If you want to understand what these forecasts mean for your plans and what’s happening on Cape, let’s connect. You can always find us 508-388-1994 (Mari and Hank) or 781-264-5517.

We’re ready to help.

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

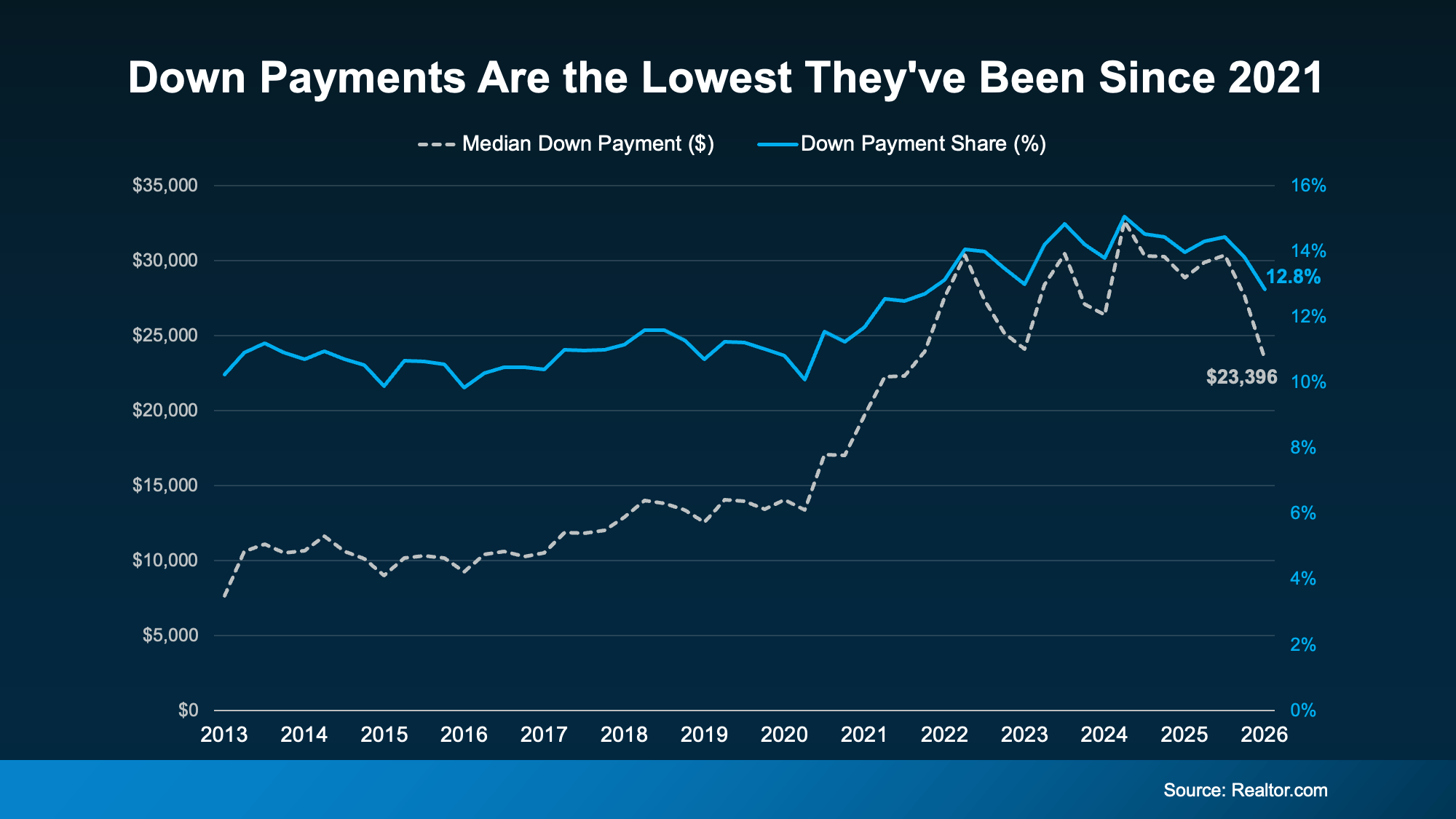

Every dollar counts when you’re buying a home, which is why the recent dip in typical down payments really matters.

According to Realtor.com, the typical buyer put down about $23,400 in early 2026 – that’s $5,000 less than in 2025 and a 19% drop year over year! That’s the lowest down payments have been since 2021(see graph below):

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

There are a few things driving the trend:

Less competition between buyers. Part of it comes down to a more balanced market. With buyers facing less competition than they did a few years ago, there’s less pressure to put a big sum down just to stand out.

More moderate home prices. Your down payment is a percentage of the purchase price. So, as price growth cools, the amount you need to put down may change too. In a lot of markets, prices have slowed or leveled off, and some areas are even seeing slight dips. That can translate into smaller down payments.

Buyers opting for loans with lower down payments. More buyers are also turning to government-backed loans, like FHA and VA, which often need little or no money down. FHA loans have made up more than 24% of purchase mortgages for five straight quarters, and VA loans recently hit their highest share in over a decade, according to Mortgage Professional America.

But even a smaller down payment is still a significant chunk of cash, and saving it can be hard. So where does the rest come from? For many buyers, two things make the difference: programs built to help, and a hand from loved ones.

Help You May Not Know You Qualify For

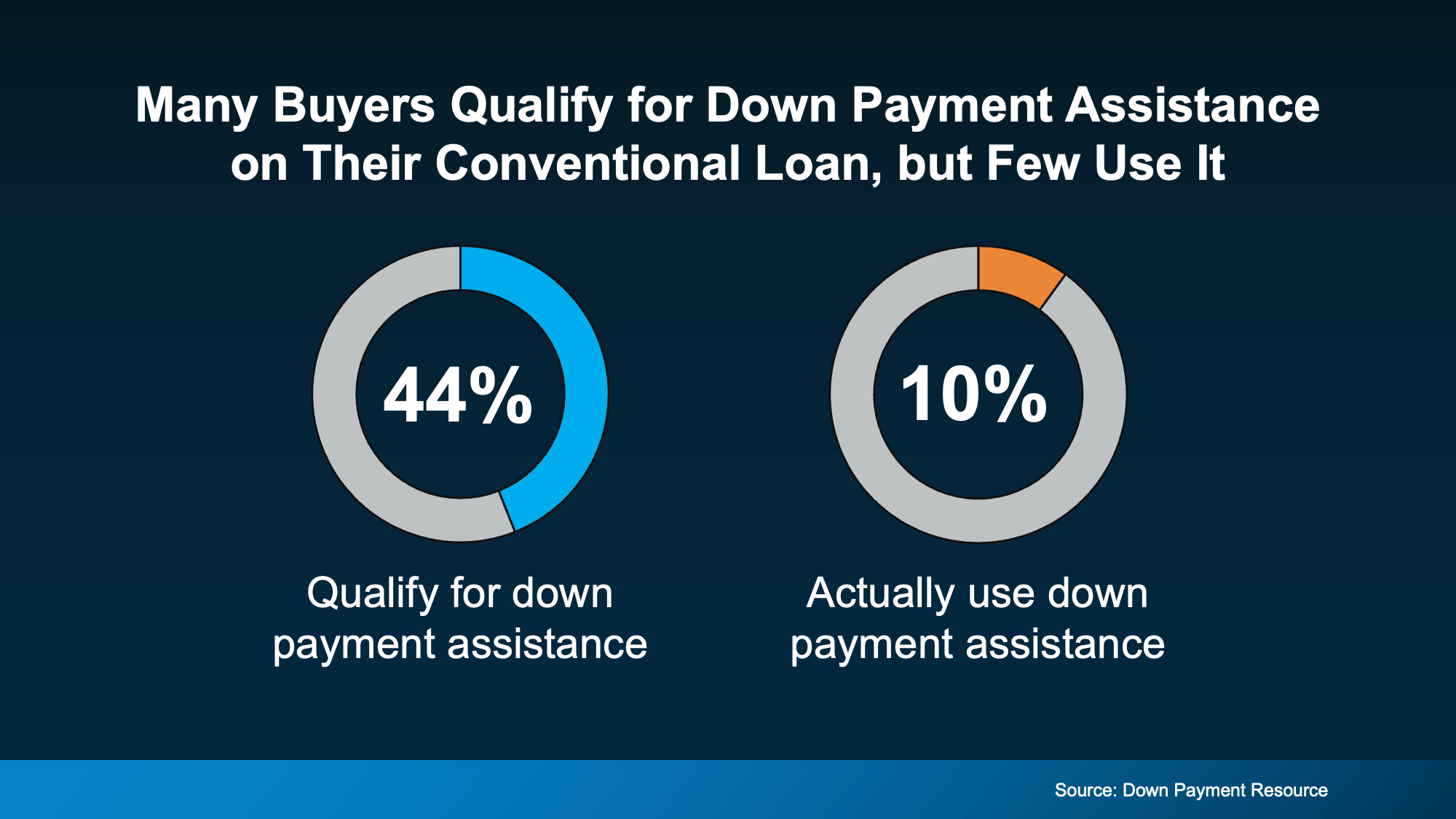

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help(see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

There are more than 2,600 down payment assistance programs available

More than half (62%) are designed to help first-time buyers

38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

62% are open to buyers earning $100,000 or more

A Boost from Loved Ones

For a growing number of buyers, help comes from closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support most often goes toward the down payment, followed by help qualifying for a mortgage and covering closing costs. Chris Birk, VP of Mortgage Insight at Veterans United, puts it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, it can make a real difference in how soon you can buy.

Bottom Line

Down payments are smaller than they’ve been in years, and that opens the door for more buyers.

And with added help from assistance programs and a little help from loved ones, you may have more ways forward than you realized.

We can help you sort through your options and connect you with a trusted lender. You can always find us at 508-399-1994 (Mari and Hank) or 781-264-5517 (Colleen).

Let’s talk soon..

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

Summer months consistently bring more sellers into the market than later in the year.

A lot of people who want to move are telling themselves the same thing: “Maybe I’ll just wait until later this year once things calm down.”

While waiting sounds like a good plan, there’s no way to know when “things will calm down.”

What we do know is that rates aren’t expected to change much, so if that’s the #1 reason you’re waiting, it may not pay off. And there could be other things you miss out on in the meantime.

Plus, you may be delaying a move that you know you have to make.

Historically, summer is one of the strongest seasons of the year for both buyers and sellers. And if you delay your move until fall or winter, some of those opportunities may already be fading.

Buyers: Fresh Inventory Is Your Real Summer Advantage

One of the biggest frustrations buyers have faced over the past few years has been a lack of affordable options. Maybe you’ve run into that yourself:

You find a house you like, but it’s out of your budget.

You find something in your budget, but you don’t like it.

Or worse, nothing interesting hits the market for weeks.

Historically, summer helps with that.

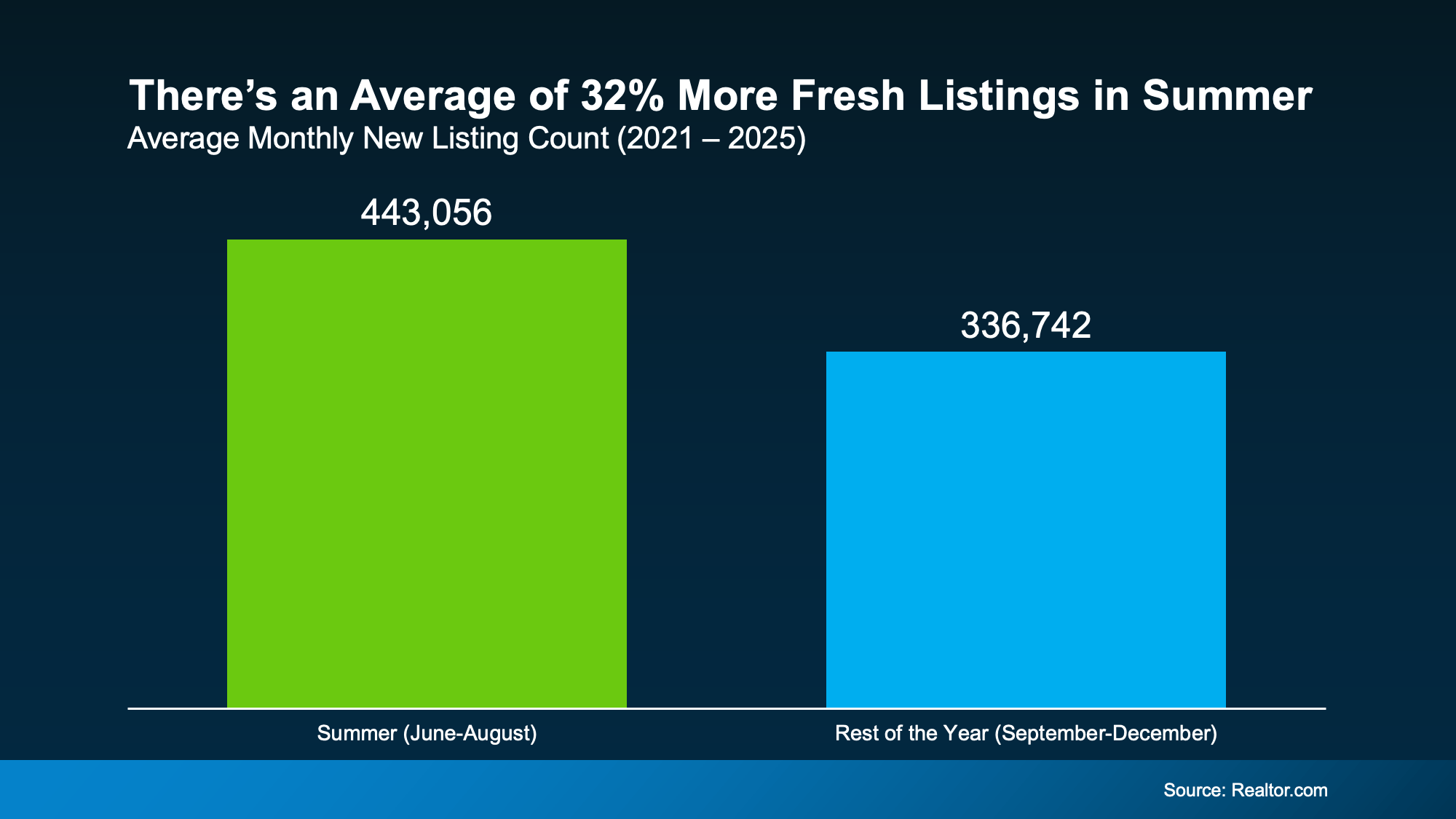

Looking at data from the last few years, summer months consistently bring more sellers into the market than later in the year. And that gives buyers a real window of fresh choices.

According to Realtor.com, any given summer month typically sees about 32% more fresh options than the average month from September-December.

With more newly listed homes, there’s a better chance of finding one you like where the numbers actually work.

Because all it really takes is one home to completely change your search. And if you’ve got more popping onto the market to choose from, maybe one of those is exactly what you need.

But keep in mind, this seasonal window isn’t open forever. Fresh inventory tends to slow down once Summer ends.

Many homeowners who planned to sell this year have already listed by then. Families who wanted to move before school starts have often already gotten it done, or at least, set it into motion. So, new listing activity usually cools as we head into fall and winter.

Of course, every year is different. But if finding the right home at the right price has been your biggest challenge, waiting until later in the year may not necessarily give you more options. In fact, recent history suggests it may do just the opposite.

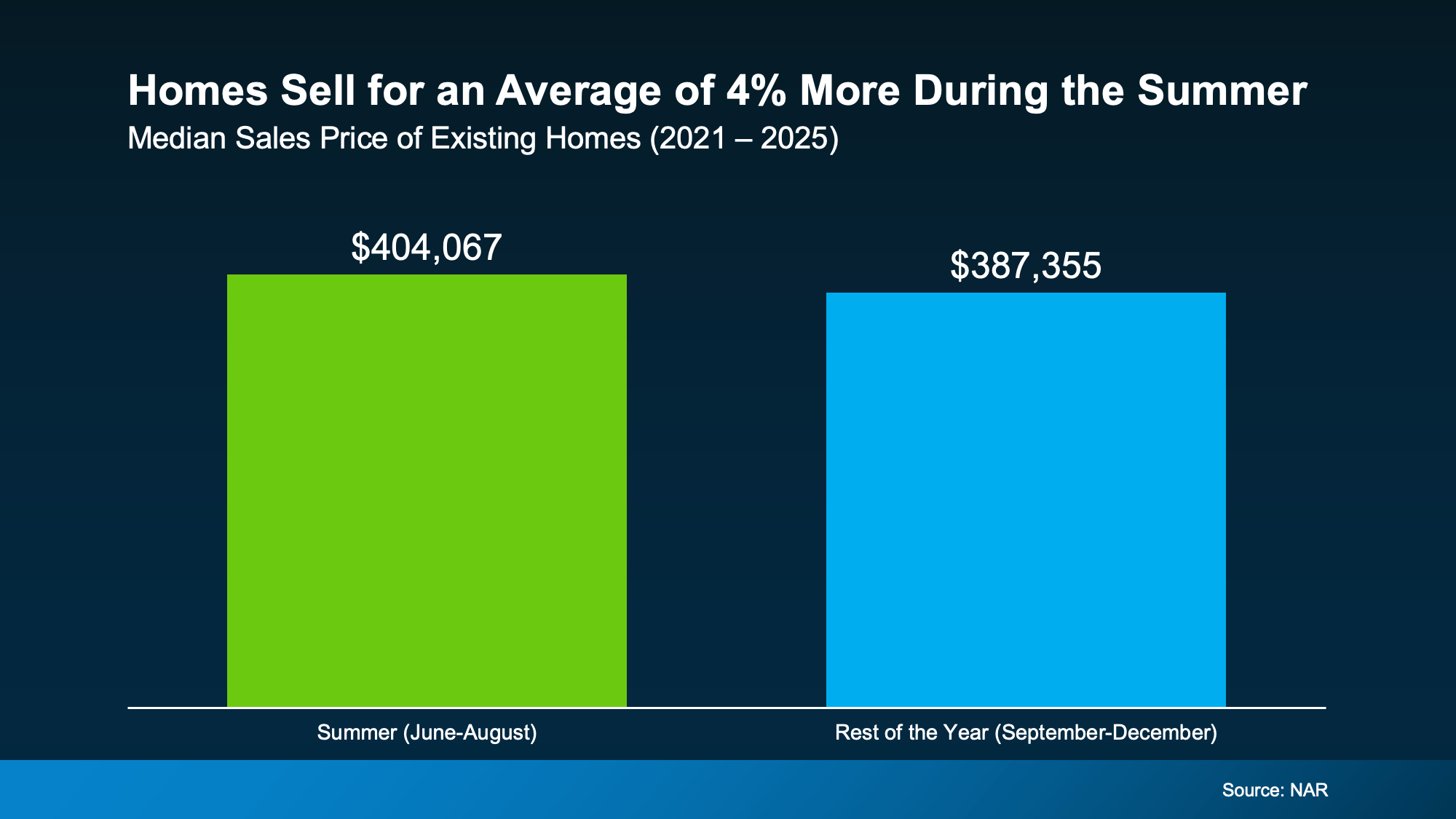

Sellers: Homes Usually Sell for More and sometimes quicker in the Summer

If you’re thinking of selling, you may be considering holding off because you’ve seen headlines about lower asking prices, price cuts, and softer conditions in some markets. But those headlines don’t tell the whole story or convey just how much it varies by area.

Here’s what you really need to know. Even though the market’s becoming more balanced and some pockets are experiencing price declines, that doesn’t mean you’ve missed your chance to sell.

Seasonality can still work in your favor no matter where you are. And this Summer could still give you the chance to sell for a good price.

According to the National Association of Realtors (NAR), homes sold during a summer month usually sell for about 4% more than homes sold during the typical month from September-December:

Why? Summer buyers are usually operating on a set timeframe. They’re trying to move before the next school year or when they have more PTO and warmer weather to tour houses. That urgency can translate into better offers.

Now, that doesn’t mean you should price your house 4% higher this summer. That would actually be a mistake in today’s market.

It just means if you’re looking to get as much for your house as you reasonably can, a summer move could be a smarter play than waiting until later this year.

Because based on typical seasonality, you may get more for your house than you would if you waited until the fall or winter (when there are typically fewer buyers active).

And if you’re considering a move anyway, that’s worth factoring in.

Bottom Line

Could waiting until later this year work out? Sure. But it’s important to understand what you may gain by moving now too – that way you have the full picture before you decide.

If a 2026 move is on your radar, let’s connect and talk about what matters most to you. You can always find us at 508-388-1994 (Mari and Hank) or 781-264-5517 (Colleen).

Depending on your priorities, summer could be your moment.

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

If the housing market feels confusing right now, you’re not the only one.

Mortgage rates have risen. Home sales haven’t picked up as much as expected. And many buyers and sellers are wondering when things are going to feel easier or be more affordable.

The truth is: a lot changed over the first half of this year.

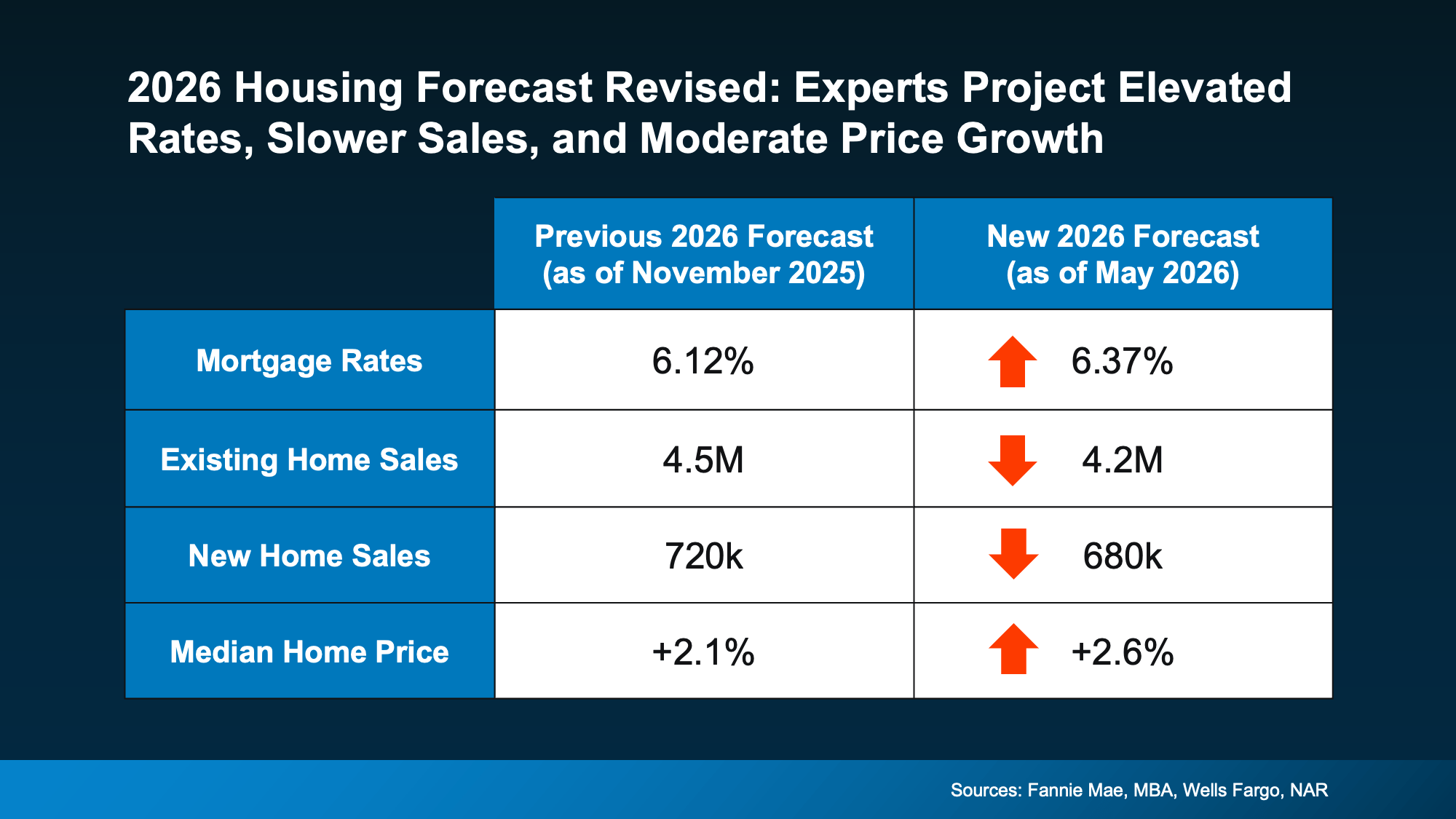

Back at the end of 2025, economists were forecasting a much stronger housing market for 2026. They expected mortgage rates to come down, affordability to improve more dramatically, and home sales to rebound.

But inflation, economic uncertainty as evidenced by increased gas and grocery prices, and continuing conflict in the Middle East have combined to push mortgage rates higher than expected. And because rates are staying elevated for longer, some buyers are continuing to hold off.

That’s why the real experts have recently revised their forecasts for the rest of the year (see graph below):

So, what does this actually mean for you? Let’s break it down.

Mortgage Rates May Remain Elevated

While just about everyone wants mortgage rates to go back to the uppers 5s or low 6s we saw at the start of the year, as of right now, the experts don’t think that’s likely to happen this year.

Instead, forecasts have been updated from the low 6s as originally projected. Many industry organizations are saying rates will stay in roughly the mid 6s this year. The good news is, that’s still lower than rates were a year ago.

Of course, this is based on what we know today. If the conflict overseas comes to an end or inflation drops, this could change. But if you’re waiting for lower rates, it may not pay off in the way you expect.

Existing Home Sales Revised Lower

Back in late 2025, experts expected we’d sell an average of 4.5 million homes this year. Now? That’s dropped down a bit to 4.2 million.

That tells us something important: buyers are still hesitant because affordability remains challenging.

Higher mortgage rates have made monthly payments harder to manage, especially for first-time buyers. And that’s slowed the pace of the market compared to what was originally expected. But even though the forecast was revised down, we’re still expected to sell more homes than last year.

Once geopolitical tensions resolve and rates begin to settle down, many experts believe that group of buyers will be ready to jump back in. As Lawrence Yun, Chief Economist at NAR, explains:

“There is sizable pent-up demand that could be released into the market.”

There already have been a few glimmers of renewed hope. In recent months, pending homes sale have been improving month over month despite higher rates.

So, if you’re able to afford a home at today’s rates, it could still make sense to buy now. Otherwise, if you wait, you’ll have more competition (and potentially fewer homes to choose from) when those other buyers jump back in.

New Home Sales Also Slowed

Builders also expected to have a stronger year. Earlier forecasts projected new home sales would top 700k in 2026. Now, economists expect we’ll be just shy of that.

Again, mortgage rates are a major reason why.

But the upside for buyers is that builders may be even more motivated to sell. That means builder incentives, negotiation opportunities, and pricing flexibility may continue.

Builders could be more ready to negotiate, and that gives you more leverage to get a better deal.

Home Prices Are Still Expected To Rise

This is one of the most important takeaways from the entire forecast. Even though sales activity is slower, on average, experts did notrevise their home price forecast downward.

They still expect prices to rise nationally this year.

Why? Because while buyer demand has softened, the number of homes for sale is still relatively limited overall. That imbalance is helping support prices, even in a slower market.

On Cape Cod, prices remain steady. In many cases, what’s being interpreted as a “drop in prices,” is actually sellers accepting the fact that this is not just a few years ago when it seemed one could list their house at just about any price and find a ready buyer.

And while buyers may think they want to see a drop in prices, generally you feel better about a big purchase when it doesn’t depreciate right away.

Bottom Line

The housing market hasn’t rebounded as quickly as experts originally hoped. But that doesn’t mean it’s stalled.

So don’t see this revision in forecasts as a sign of trouble. See it as a temporary reaction to overall conditions and uncertainty.

If you have selling — or buying — on your mind, we’re happy to walk you through your options. You can always find us at 508-388-1994 (Mari and Hank) or Colleen (781-264-5517.)

Let’s talk soon…

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

You may be telling yourself that you’re going to wait to move – maybe you’re hoping mortgage rates will come down, prices will fall, or the market will feel a little easier.

And honestly? A lot of people are feeling that way right now. But here’s what some are starting to realize.

Waiting doesn’t usually fix the thing that made you want to move in the first place.

Your family still desperately needs more room. Your empty nest still feels too…empty.

Your parents or grandparents still need you to live closer.

You just got married… or divorced.

Your vision of retirement has you living somewhere else.

Eventually, life can reach a point where waiting feels harder than moving.

That’s why some people are still deciding to buy right now, even in today’s market. Not because conditions are perfect. But because the life changes behind their move never really went away.

And maybe that’s exactly where you are too. If so, you’re certainly not alone.

The Real Reasons People Move

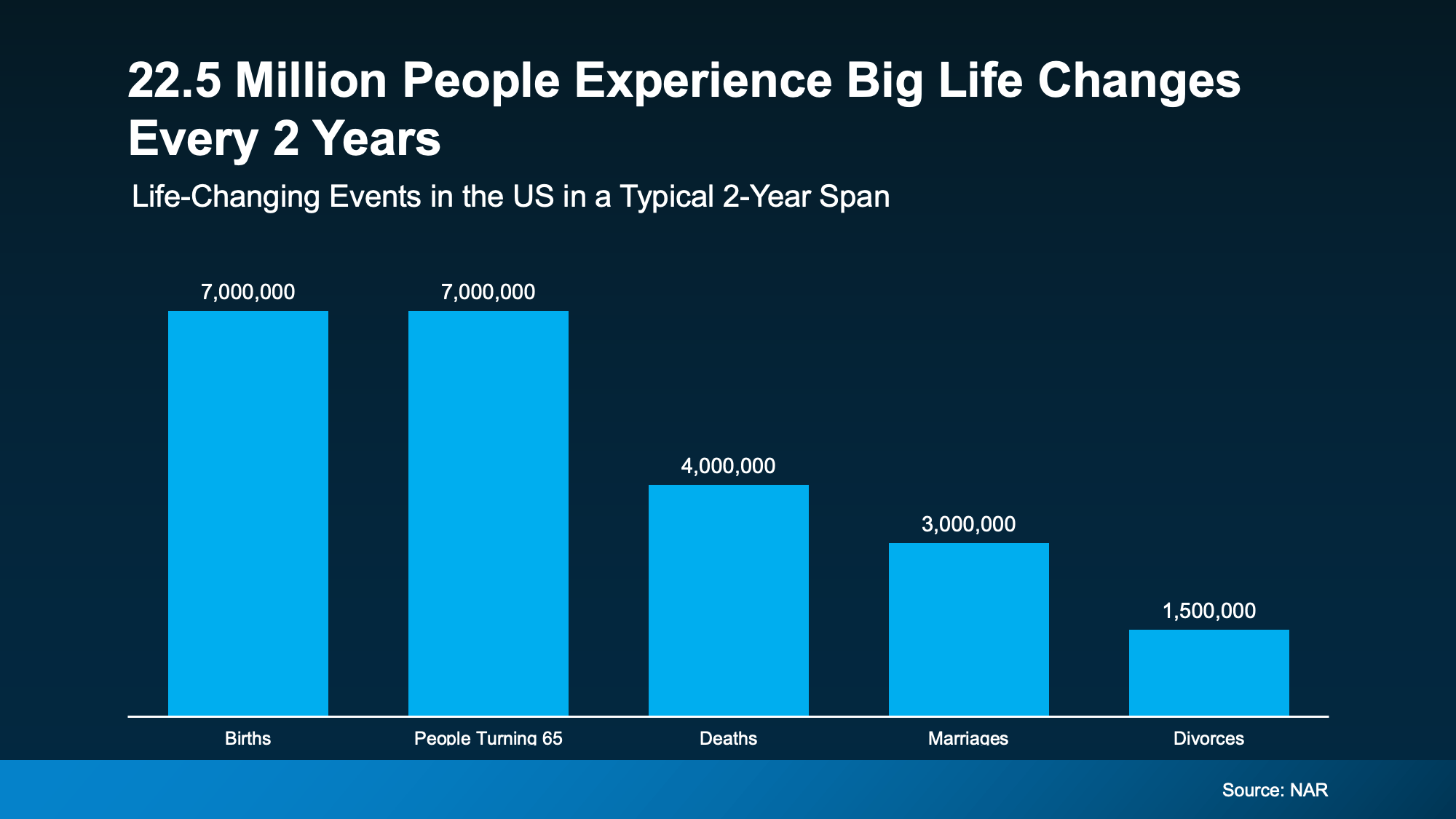

Data from the National Association of Realtors (NAR) shows 1 in 5 buyers last year said they felt like they had to purchase a home at that time, no matter the market.

That’s an important reminder right now. Sure, the dollars and cents of your move have to make sense for you. But big life changes happen whether mortgage rates and home prices are high, low, or somewhere in between.

And those big life events happen more than you may think. NAR says roughly 22.5 million people experience major life changes in a typical two-year span (see graph below):

These are exactly the kinds of things that can change how much space you need, where you want to live, or what kind of lifestyle makes sense now. Chen Zhao, Head of Economics Research at Redfin, explains:

“Life doesn’t stand still—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood.”

And that’s what makes waiting so hard. Every month you spend hoping the market changes is another month living in a house that no longer works for your life. It’s stressful to feel stuck. And that feeling usually doesn’t disappear.

There May Be More Opportunity Than You Think

But while affordability is still a challenge, there may still be a way for you to make your move.

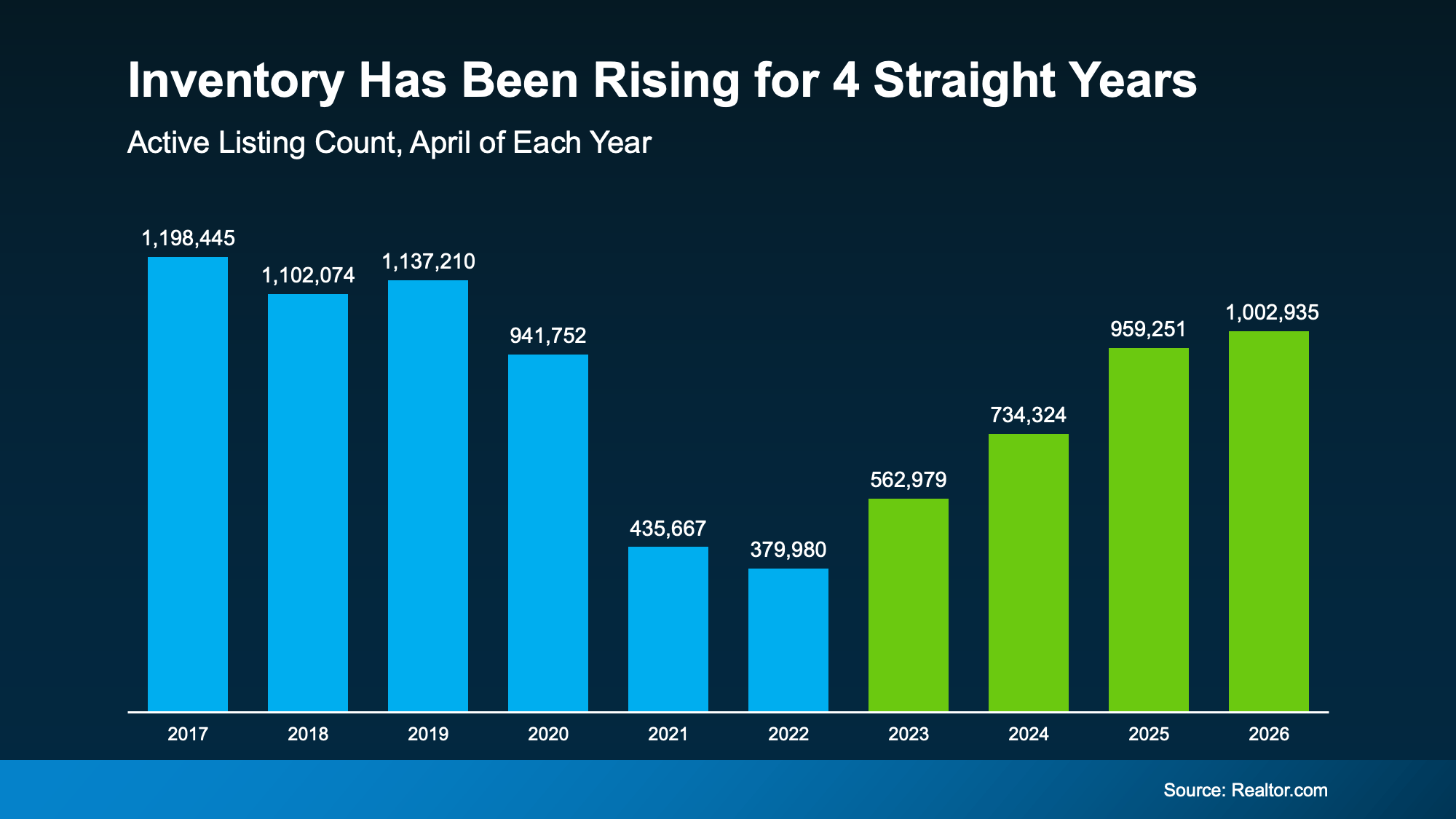

The number of homes for sale has been growing for 4 straight years (see graph below). That means more homes to choose from, and, in some markets, more room to negotiate than buyers had just a few years ago.

That doesn’t mean moving is suddenly easy. But it does mean some buyers are finding ways to make a move work. So, if you’ve been putting your plans on hold, maybe the question isn’t just:

“What’s the market doing?” or “When will it get better?”

Maybe ask yourself this, too: “Can I still live where I’m at right now and make it work?”

If the answer to that second question is “no,” it may be worth having a conversation about what your options look like today – despite where rates or prices are. You could find your move is still possible after all. With more homes for sale, there’s a better chance to find one that fits your life (and your budget) right now.

Bottom Line

Life changes. Priorities shift. Families grow. Kids move out. Careers evolve. And eventually, the house you’re in may stop fitting the life you’re living.

If that’s been weighing on you lately, let’s talk through what your options could realistically look like today, no matter where rates or prices are. You can always find us at 508-388-1994 (Mari and Hank) or 781-264-5517 (Colleen).

Life can’t always wait for perfect market conditions. Maybe you don’t have to either.

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

For a lot of potential first-time home buyers, affordability is what’s standing in their way. But some buyers are getting creative and finding a way to still make the numbers work – and that’s through co-buying.

The Dream Is Still Alive. The Math Just Isn’t Working for Everyone.

Young people haven’t given up on the dream of owning a home – not even close. According to FirstHome IQ, homeownership still ranks among the top life goals for the next generation.

The problem? 73% of Gen Z and millennial buyers cite affordability as the reason for not making homeownership a priority. And it shows. First-time buyers now make up just 21% of all home purchases, the lowest share since the National Association of Realtors (NAR) started tracking the data in 1981.

But still, some buyers are making it happen. And a portion of them are turning to co-buying to get their foot in the door.

So, What’s Co-Buying?

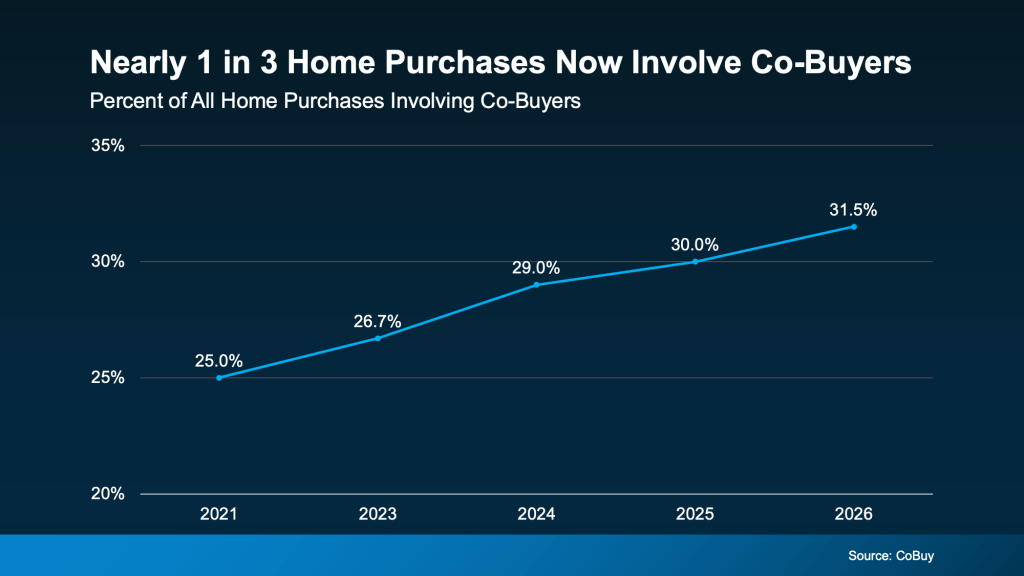

Co-buying means purchasing a home with someone else, like a friend, sibling, or unmarried partner. You combine incomes, split the down payment, and share monthly costs. For some people, it’s a creative way to turn “someday” into a concrete move-in date that’s just around the corner.

And it’s catching on fast, just look at where things stand today. According to CoBuy.io, 64 million Americans now co-own a home with someone they’re not married to. In fact, 31.5% of home purchases involve co-buyers (see graph below):

Why It Works

Here are just a few of the top reasons buyers are going this route, according to NerdWallet:

Quicker path to homeownership: If owning a home is a serious goal for you, buying with someone else can help make that reality on a shorter timeline. Two or more people can save up a down payment a lot faster than one. That’s less time waiting and more time building equity in a place that’s yours.

More purchasing power: With multiple incomes going toward the home purchase, you might be able to afford a nicer home or live in a more popular neighborhood. Sometimes teaming up means getting the home you actually want, not just the one you can barely afford on your own.

Easier loan qualification: Added income from more than one buyer can also help with your debt-to-income (DTI) ratio, which the lender will calculate based on all the borrowers.

Lower housing costs: Splitting up a mortgage payment multiple ways could maybe even make owning less expensive than renting Plus, sharing costs can make repairs or renovations more manageable, too.

Things To Keep in Mind

If you’re considering going this route, there are some things you’ll want to think over. For starters, co-buying works best with people you trust and share financial goals with. So, before moving forward, make sure everyone agrees on how costs are split, who handles what, and what happens if one person wants to sell down the road.

That’s why a written co-ownership agreement can be a smart move. It keeps everyone on the same page and helps avoid headaches down the line. Think of it less like a legal formality and more like a game plan for your new investment.

Bottom Line

Affordability challenges are real, but they don’t have to mean waiting indefinitely. Co-buying is helping some first-time buyers stop waiting and start putting down roots.

If you’re curious whether it could work for your situation, let’s talk. Reach out today and let’s figure out your path to homeownership together. You can always find us at 508-388-1994 (Mari and Hank) and 781-423-8662 (Colleen).

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

Some buyers, sellers, and commentators are a little uncertain right now about the housing market. And that’s led to some dramatic headlines. If you’re thinking about buying a home, this may be making you feel a little uneasy about your decision.

A recent study by CNBC asked homebuyers what they’re most worried about, and three themes kept coming up again and again:

Mortgage rates

The number of homes for sale

Home prices

You should know that a lot of what you may be hearing is based more on misconceptions than facts. So, let’s break it down and separate fact from fiction.

Misconception #1:“I’ll Just Wait, Because Mortgage Rates Are Going To Fall Dramatically”

One idea going around on social is that mortgage rates are going to drop dramatically soon. So, it’s better to wait to buy.

But is thatreallywhat’s expected?

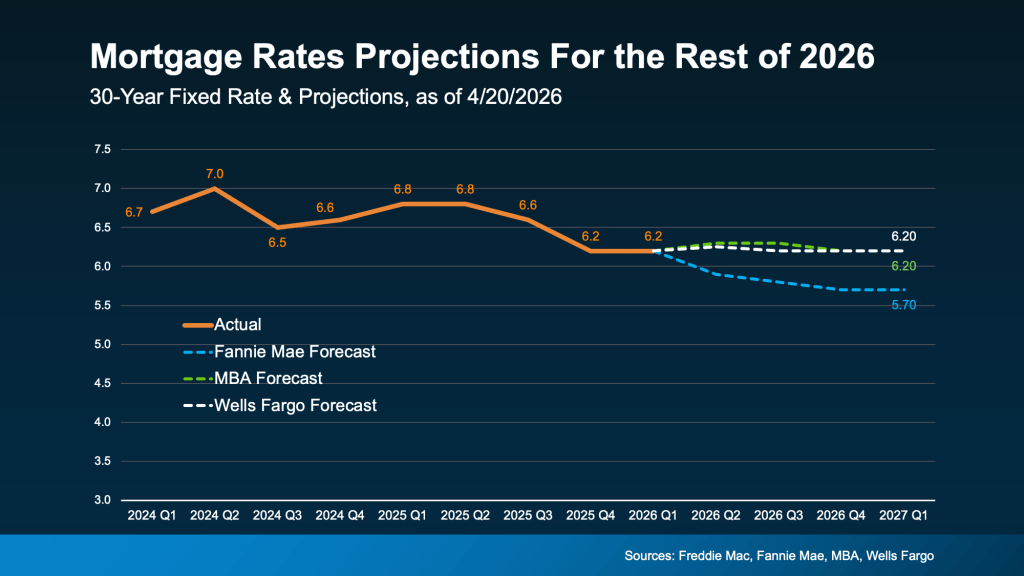

While mortgage rates have come down a bit in the last few weeks, forecasts don’t show a major drop ahead.The most likely scenario is that rates stay somewhere in the low 6% range this year.

And that’s not a big change from where rates are now (see graph below):

Of course, this depends on where inflation and the economy go from here. But, based on what we know today, waiting for a big drop in rates may not work out the way some people hope. AsU.S. Newsexplains:

“Mortgage rates aren’t expected to change much over the next several quarters . . .”

Not to mention, even with rates where they are today, it’s alreadymore affordable than a year ago. So, even if they don’t change much, it’s still better than it was.

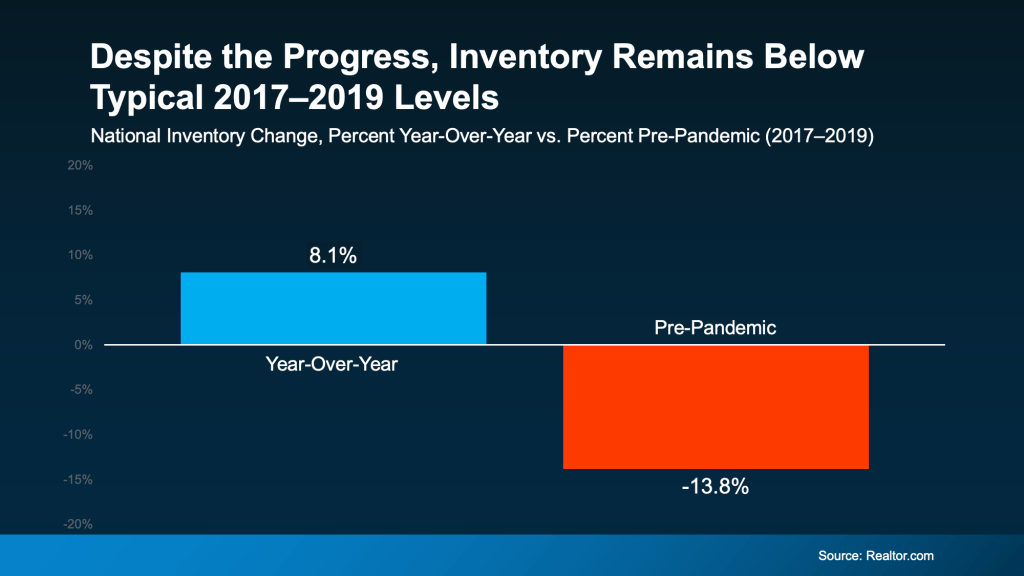

Misconception #2:“There Are Too Many Homes for Sale Right Now”

You’ve probably heard inventory is up. And nationally, it is. The number of homes for sale is 8% higher than this time last year. But that’s not a bad thing. In fact, it’s one of the reasons buyers have a bit morebreathing room right now.

The problem is the headlines are making something good, sound bad. They’re focusing on how this is the most inventory we’ve had since 2019 or how many homes builders are building. And that can make it sound like the number of homes for sale is rising too far, too fast.

But that’s not what the bigger picture shows.

DatafromRealtor.comshows that, even though inventory is up compared to last year, it’s still nearly 14% lower than it was during the last normal housing market (2017-2019):

On Cape Cod, inventory is down 21% comparing this March to last.

Misconception #3:“Home Prices Are About to Crash”

You’ve probably seen this one, too. The confusion is coming from the fact that some areas are experiencing price declines. And influencers are running with that and saying prices are crashing. But that’s not the reality.

Most areas are seeing prices rise, not fall. On Cape, the median sales price for a single-family home is up almost 2% YTD comparing the first three months of this year with the same time period in 2025.

Why are prices up?

Many homeowners aren’t selling because they don’t want to give up the low mortgage rate they locked in a few years ago. And that’s keeping a lid on how much inventory can grow.

Since inventory is still below pre-pandemic norms, there aren’t enough homes for sale to cause a price crash.

And even in markets with more inventory, some sellers are choosing to pull their homes off the market instead of cutting prices.

Bottom Line

Online posts are going to make things sound worse than they are. If you want a true, data-bound look at what’s really happening in today’s market, please talk with us. You can always find us at 508-388-1994 (Mari and Hank) or 781-423-8662

We can separate fact from fiction.

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

The math on buying a home doesn’t seem to be adding up right now for some folks. Maybe that’s how it feels for you, as well. You look at the cost of buying. Then you look at the cost of expenses like childcare. And it starts to feel as if you need to choose between one or the other.

But some families are finding a way to work things out by doing something a little different: teaming up with family members to purchase a multi-generational home.

One Reason This Is Becoming More Common

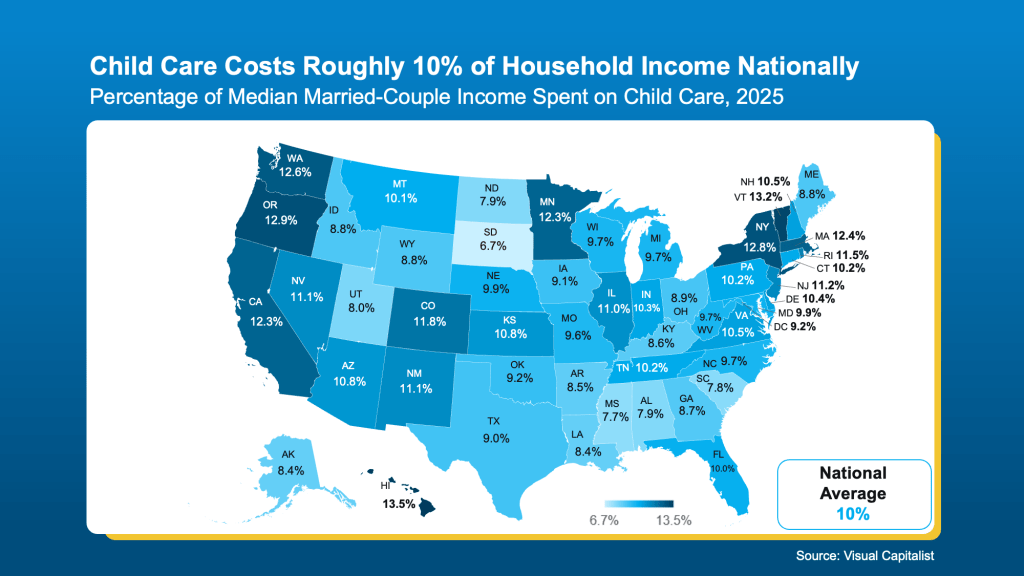

It’s no secret that affordability has been a challenge in recent years. But for families with young kids, there’s an added layer that can make it feel even harder: childcare.

According to the Department of Health and Human Services, childcare should take up no more than 7% of your monthly income. But in reality, the average married couple spends closer to 10%. In Massachusetts, it’s almost 12.5%. (see map below):

When you combine that with the cost of buying a home, it’s easy to see why things can feel stretched. That’s exactly why more families are starting to rethink how they approach both.

The Solution More People Are Turning To: Multi-Generational Living

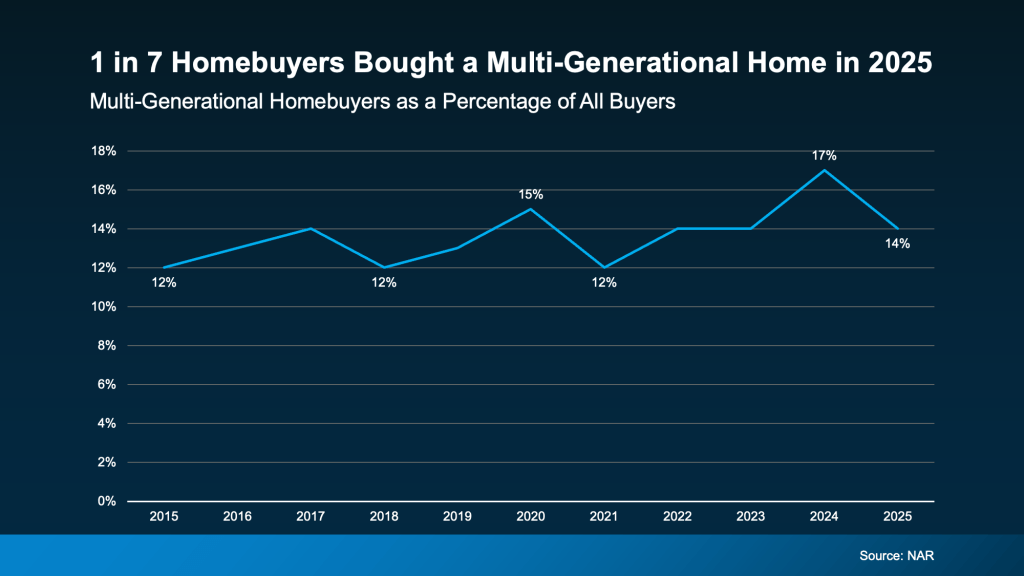

One option gaining traction? Multi-generational living. That’s when parents, grandparents, or other relatives buy a house together and live under the same roof. And it’s not just about convenience anymore. It’s becoming a go-to strategy.

You can see it in the data. According to the National Association of Realtors (NAR), almost 1 in 7 homebuyers (14%) bought a multi-generational home in 2025 (see graph below):

And for the first time, childcare is showing up as a key reason why they chose this option. As NAR explains:

“This year’s report features two new primary reasons for purchasing a multi-generational home: grandchildren living in the home (12%) and to help reduce the cost of childcare (6%).”

Why It Works

Buying a multi-generational home solves two big challenges at the same time.

First, it shares the financial responsibility. If you pool multiple incomes together, you may be able to afford a home you couldn’t have on your own.

Second, it can also solve the childcare puzzle. When grandparents or other relatives live in the home, they may be able to help with daily care – which can significantly reduce or even eliminate daycare costs.

And for many people, that combination is what finally makes their move possible.

If the costs of childcare and housing together have made buying feel out of reach right now, it may be worth exploring creative options like buying a home with your loved ones.

Bottom Line

If you want more information on multi-generational homes, let’s have a quick conversation about some possible options. You can always find us at 508-388-1994 (Mari and Hank) and 781-423-8662 (Colleen).

Sometimes the path to homeownership isn’t doing it alone. It’s doing it together.

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.