The math on buying a home doesn’t seem to be adding up right now for some folks. Maybe that’s how it feels for you, as well. You look at the cost of buying. Then you look at the cost of expenses like childcare. And it starts to feel as if you need to choose between one or the other.

But some families are finding a way to work things out by doing something a little different: teaming up with family members to purchase a multi-generational home.

One Reason This Is Becoming More Common

It’s no secret that affordability has been a challenge in recent years. But for families with young kids, there’s an added layer that can make it feel even harder: childcare.

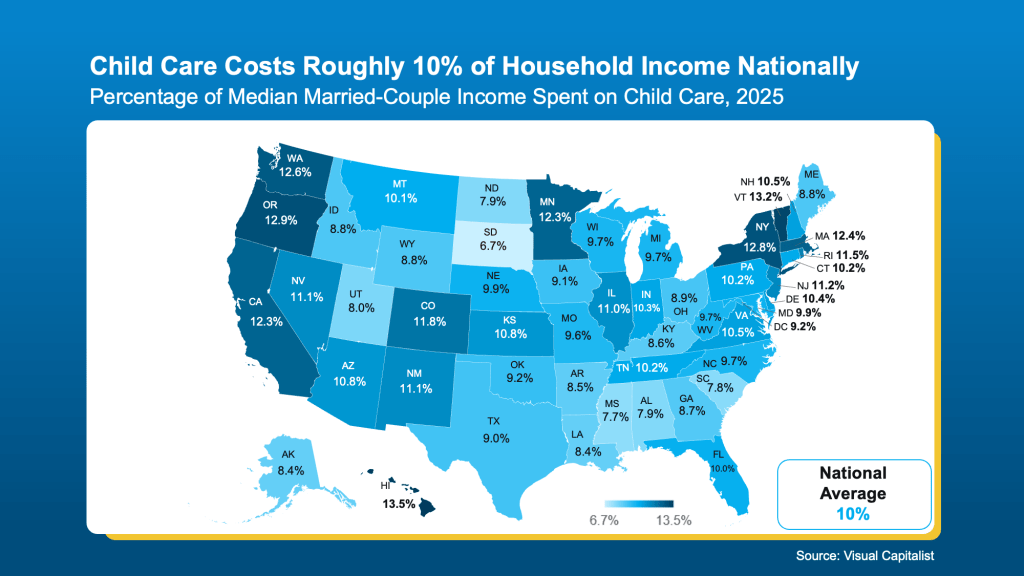

According to the Department of Health and Human Services, childcare should take up no more than 7% of your monthly income. But in reality, the average married couple spends closer to 10%. In Massachusetts, it’s almost 12.5%. (see map below):

When you combine that with the cost of buying a home, it’s easy to see why things can feel stretched. That’s exactly why more families are starting to rethink how they approach both.

The Solution More People Are Turning To: Multi-Generational Living

One option gaining traction? Multi-generational living. That’s when parents, grandparents, or other relatives buy a house together and live under the same roof. And it’s not just about convenience anymore. It’s becoming a go-to strategy.

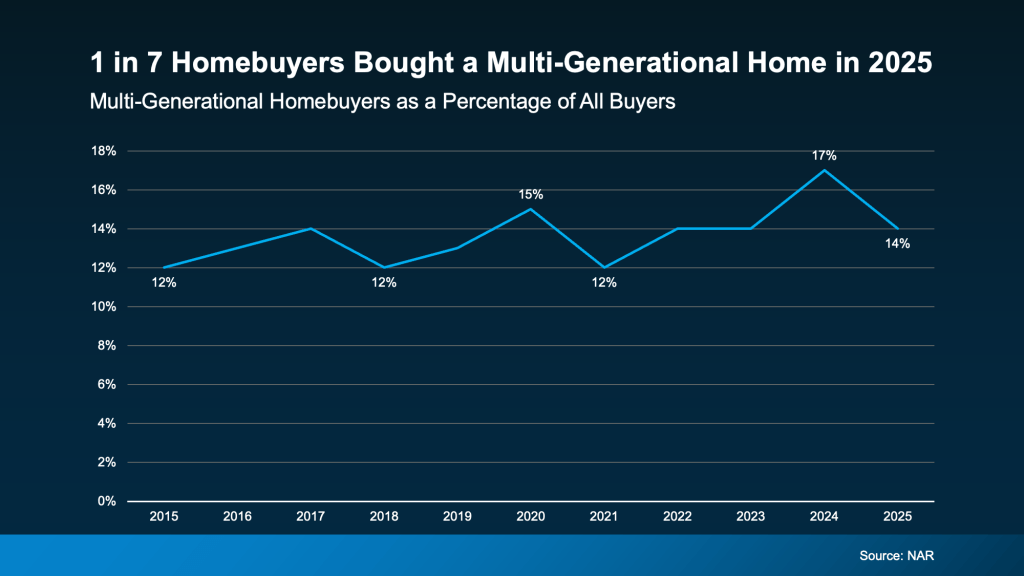

You can see it in the data. According to the National Association of Realtors (NAR), almost 1 in 7 homebuyers (14%) bought a multi-generational home in 2025 (see graph below):

And for the first time, childcare is showing up as a key reason why they chose this option. As NAR explains:

“This year’s report features two new primary reasons for purchasing a multi-generational home: grandchildren living in the home (12%) and to help reduce the cost of childcare (6%).”

Why It Works

Buying a multi-generational home solves two big challenges at the same time.

- First, it shares the financial responsibility. If you pool multiple incomes together, you may be able to afford a home you couldn’t have on your own.

- Second, it can also solve the childcare puzzle. When grandparents or other relatives live in the home, they may be able to help with daily care – which can significantly reduce or even eliminate daycare costs.

And for many people, that combination is what finally makes their move possible.

If the costs of childcare and housing together have made buying feel out of reach right now, it may be worth exploring creative options like buying a home with your loved ones.

Bottom Line

If you want more information on multi-generational homes, let’s have a quick conversation about some possible options. You can always find us at 508-388-1994 (Mari and Hank) and 781-423-8662 (Colleen).

Sometimes the path to homeownership isn’t doing it alone. It’s doing it together.

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.