Every dollar counts when you’re buying a home, which is why the recent dip in typical down payments really matters.

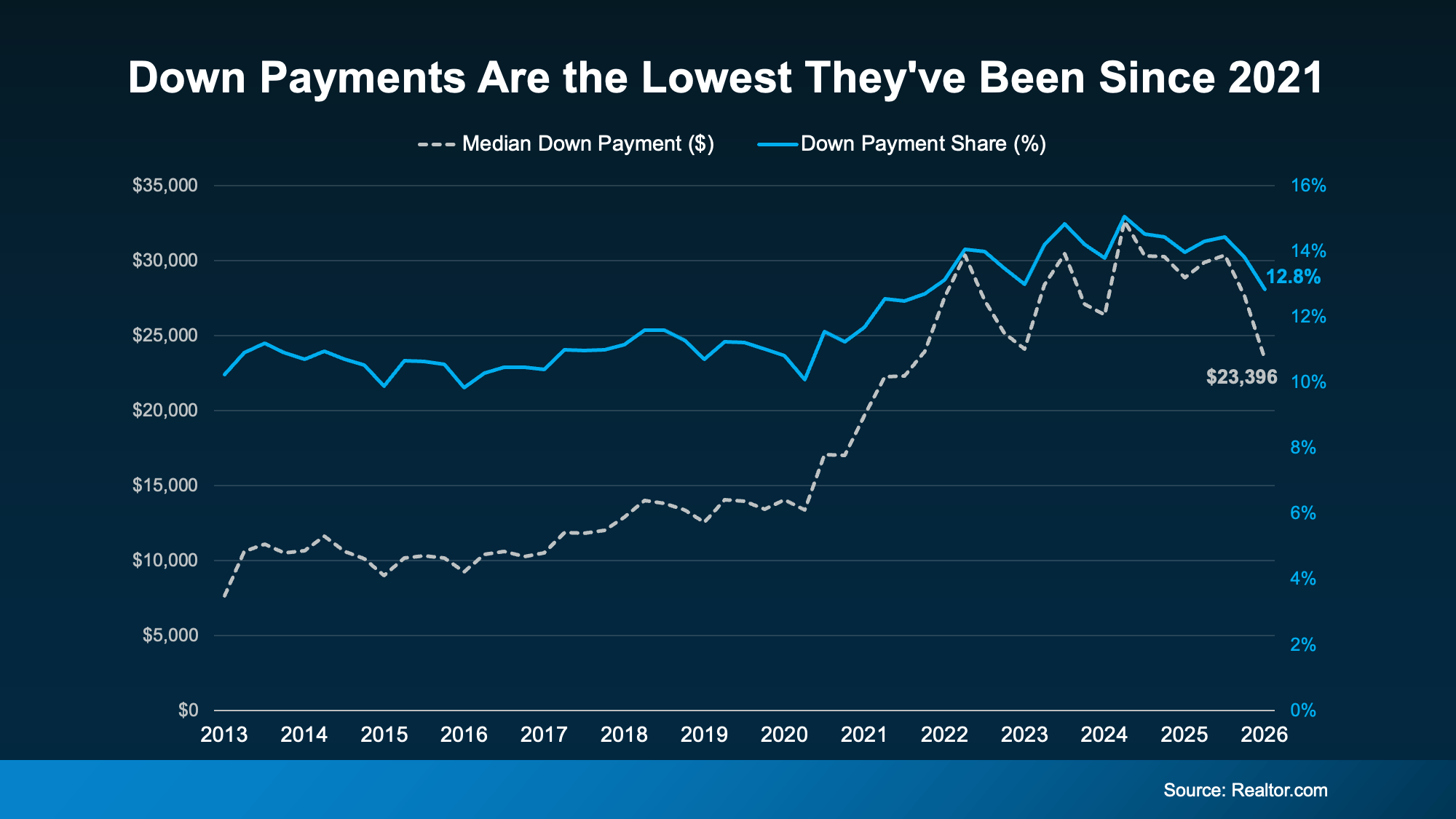

According to Realtor.com, the typical buyer put down about $23,400 in early 2026 – that’s $5,000 less than in 2025 and a 19% drop year over year! That’s the lowest down payments have been since 2021 (see graph below):

So why are buyers putting less money down, and how can you put less down, too? Here’s your answer.

Why Down Payments Are Getting Smaller

There are a few things driving the trend:

- Less competition between buyers. Part of it comes down to a more balanced market. With buyers facing less competition than they did a few years ago, there’s less pressure to put a big sum down just to stand out.

- More moderate home prices. Your down payment is a percentage of the purchase price. So, as price growth cools, the amount you need to put down may change too. In a lot of markets, prices have slowed or leveled off, and some areas are even seeing slight dips. That can translate into smaller down payments.

- Buyers opting for loans with lower down payments. More buyers are also turning to government-backed loans, like FHA and VA, which often need little or no money down. FHA loans have made up more than 24% of purchase mortgages for five straight quarters, and VA loans recently hit their highest share in over a decade, according to Mortgage Professional America.

But even a smaller down payment is still a significant chunk of cash, and saving it can be hard. So where does the rest come from? For many buyers, two things make the difference: programs built to help, and a hand from loved ones.

Help You May Not Know You Qualify For

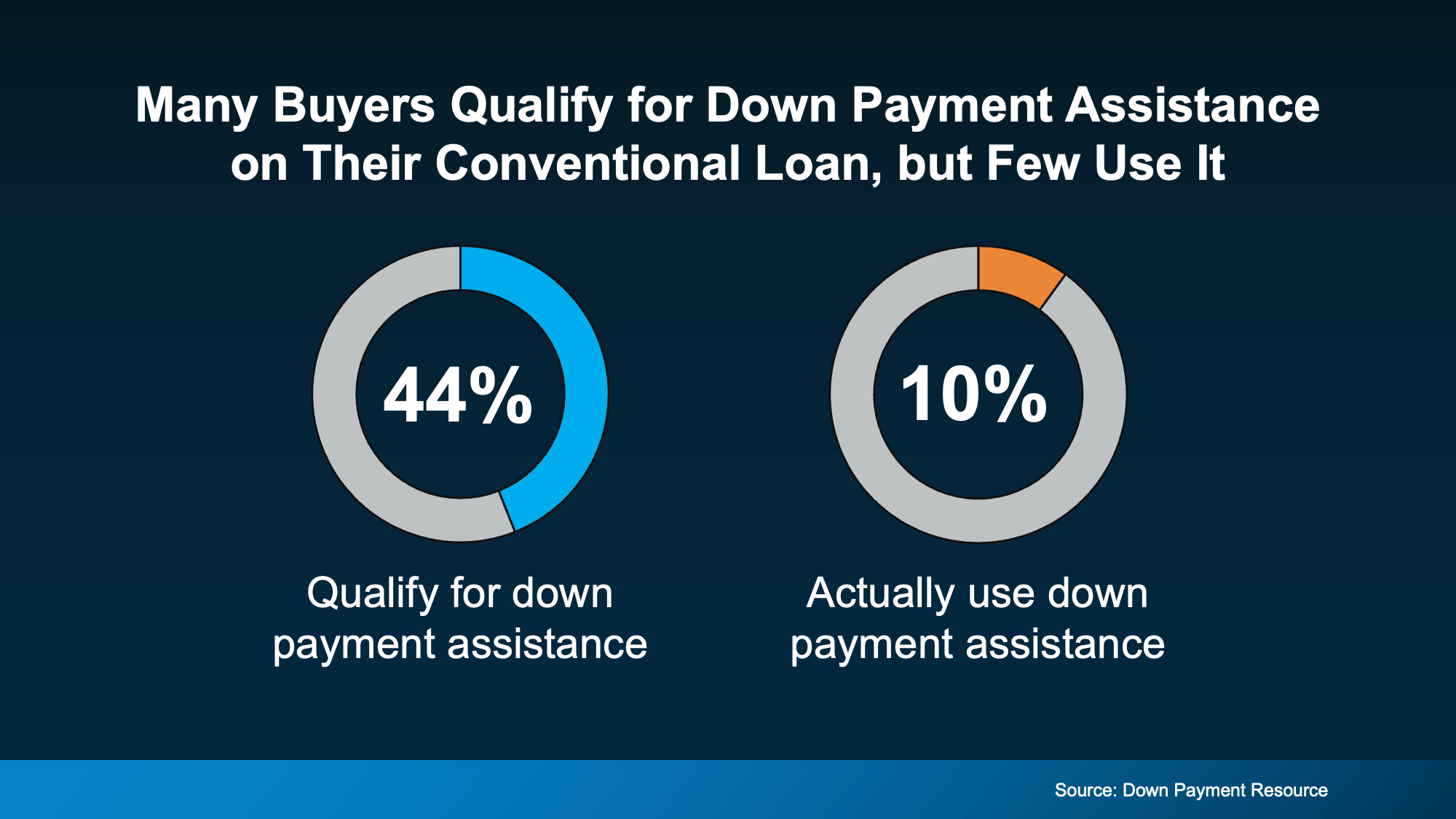

Down payment assistance is one of the most overlooked tools out there. Looking at the 10 largest U.S. metros, Urban Institute and Down Payment Resource found nearly 44% of recent buyers already qualified for a down payment program, but many of them closed on their loan without tapping the help (see chart below):

The options are broader than you might assume, too. According to Down Payment Resource:

- There are more than 2,600 down payment assistance programs available

- More than half (62%) are designed to help first-time buyers

- 38% have no first-time buyer requirement, so you may qualify even if you’ve owned before

- 62% are open to buyers earning $100,000 or more

A Boost from Loved Ones

For a growing number of buyers, help comes from closer to home. Research from Veterans United shows about 59% of parents have provided or plan to provide financial support to help their child buy a home.

That support most often goes toward the down payment, followed by help qualifying for a mortgage and covering closing costs. Chris Birk, VP of Mortgage Insight at Veterans United, puts it this way:

“For many families, helping a child buy a home has become less of an optional gesture and more of a practical response to today’s affordability challenges.”

If your loved ones are in a position to help, it can make a real difference in how soon you can buy.

Bottom Line

Down payments are smaller than they’ve been in years, and that opens the door for more buyers.

And with added help from assistance programs and a little help from loved ones, you may have more ways forward than you realized.

We can help you sort through your options and connect you with a trusted lender. You can always find us at 508-399-1994 (Mari and Hank) or 781-264-5517 (Colleen).

Let’s talk soon..

Mari, Hank, and Colleen

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.