If you stepped back from your home search over the past few years, you’re not alone.

But the good news today is that things have changed, and you might want to take another look. With more homes to choose from, prices leveling off in many areas, and mortgage rates easing, today’s market is offering something you haven’t had in a while: options.

Experts agree, buyers are in a better spot right now than they’ve been in quite a long time. Here’s what they have to say.

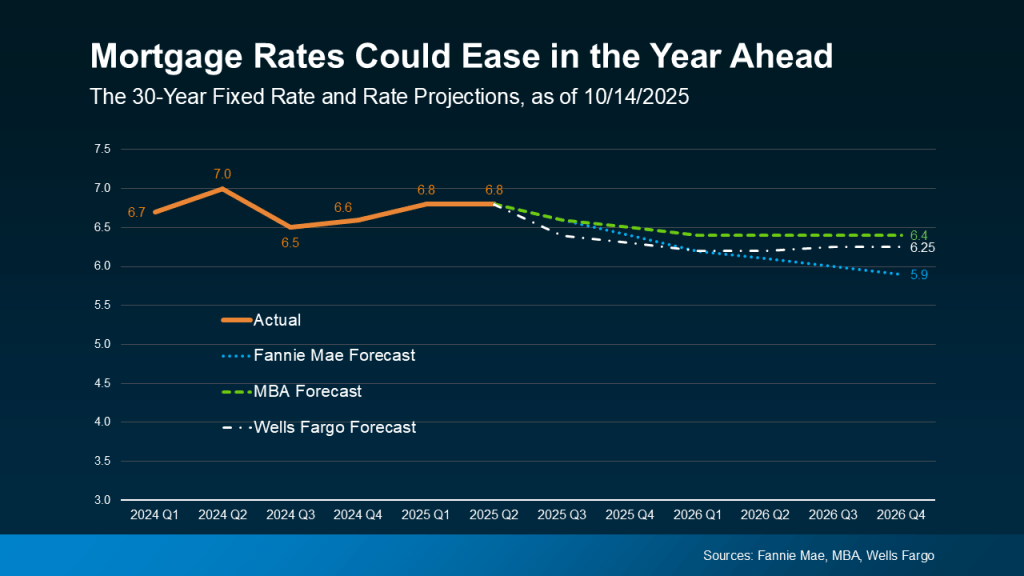

Affordability Is Finally Improving

Lisa Sturtevant, Chief Economist at Bright MLS, says affordability is finally starting to turn the corner:

“Slower price growth coupled with a slight drop in mortgage rates will improve affordability and create a window for some buyers to get into the market.”

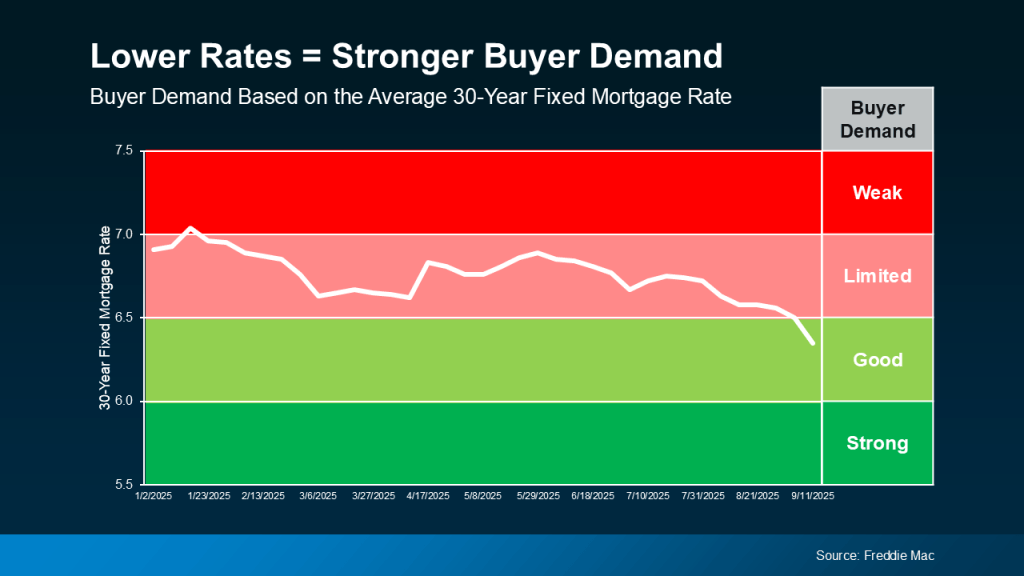

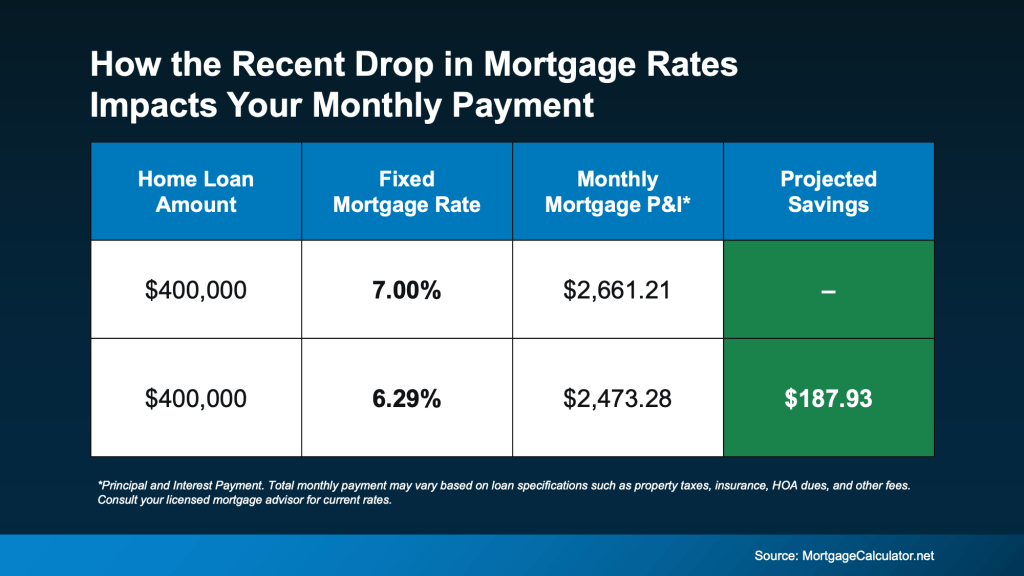

Mortgage rates have eased from their recent highs, price growth has slowed, and that one-two combo is making homes more affordable than they’ve been in months.

And please don’t get discouraged when you see what the “median sales price” is. The median is the price in the middle. There are just as many homes for sale below that number as above.

There Are More Homes on The Market

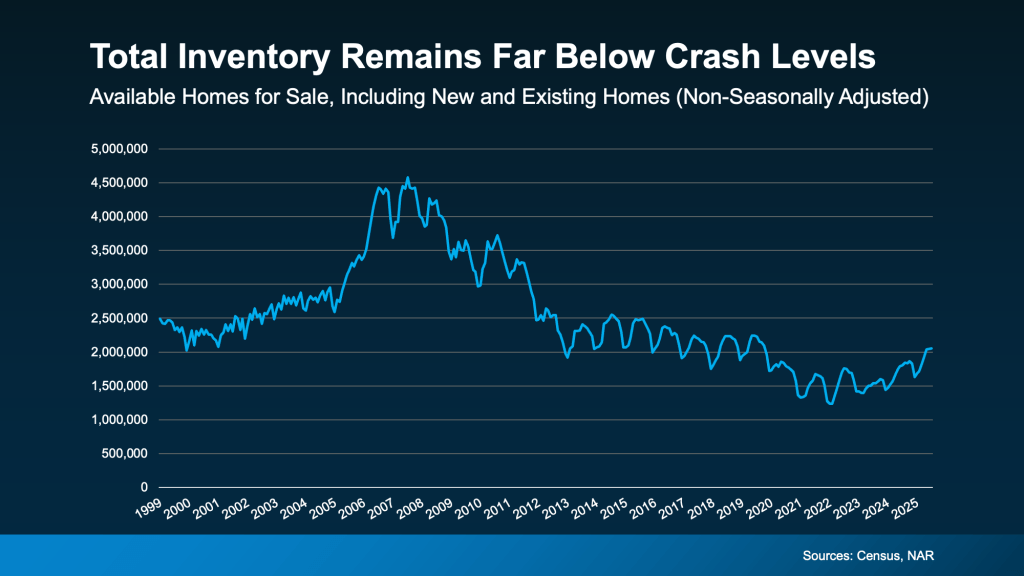

Prices are easing because there are more homes on the market. According to the latest from Realtor.com, there are 17% more homes for sale today than there were at this time last year. That means more options, less competition with other buyers, and a chance to find the space that actually works for you.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Homebuyers are in the best position in more than five years to find the right home and negotiate for a better price. Current inventory is at its highest since May 2020, during the COVID lockdown.”

Take a look at the numbers.

As Yun notes, inventory is up everywhere. Compared to this time last year, every region of the country has more homes on the market than at this time last year (see graph below):

On Cape Cod, there are more homes and condos for sales, too.

So, when you step back and look at the bigger picture, this means more choices for everyone.

And with fewer buyers in the market and more homes for sale, sellers are willing to negotiate to get a deal done.

All of this adds up to a win if you’ve been thinking about buying.

If you stepped away from your search because things felt too competitive, too pricey, you were worried about finding a home, or it was all just too much to process, this could be your moment to take another look.

And if you’re not quite ready to go all in, that’s okay too. You can start by planning ahead. We’re here to work with you. We can help you break down your budget, narrow your search, and make sure you’re prepped and ready when the right home hits the market.

If prices on Cape Cod aren’t for you? Where else would you consider living? We can help you with that, too, as Today Real Estate has realtors throughout New England.

Bottom Line

Let’s talk.

Because this isn’t 2021.

This isn’t even 2023 or 2024.

This is a new market – and you might be surprised by what you could find.

Mari and Hank

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.