We’re happy to tell you that we have begun a new monthly program on Mashpee TV.

Called “How’s the Market?” — which is the question we get all the time from family, friends, and even total strangers! — we will answer that question and many others with just the facts and no spin.

In our first episode, which you can see linked below, we talk about current market data, as well as some of the most recent changes to the home buying and selling process.

We’ll have guests, as well. Our September program will feature Todd Machnik, President of Today Real Estate, as well as the President of the Cape Cod and Islands Association of Realtors. We should be heading into the studio soon to have what we’re sure will be a very informative discussion.

If you live in our hometown of Mashpee, you can see “How’s the Market?” on channel 1072.

If not, we’ll be sharing the link on our social media. The program can also be found on the Mashpee TV YouTube channel. (And our own YouTube channel soon.)

We hope you’ll watch. If you have suggestions for topics you’d like to see us cover, please let us know at 508-388-1994 or msennott@todayrealesate.com.

Buyers who are holding out for lower mortgage rates may be missing a key opening in the market.

Mortgage rates are always a hot topic – and for good reason. After the most recent jobs report came out weaker than expected, the bond market reacted almost instantly. As a result, in early August mortgage rates dropped to their lowest point so far this year (6.55%).

While that may not sound like a big deal, pretty much every buyer has been waiting for rates to fall. And even a seemingly small drop like this reignites the hope we’re finally going to see rates trending down. But what’s realistic to expect?

According to the latest projections, rates aren’t expected to fall dramatically anytime soon. Most experts project they’ll stay somewhere in the mid-to-low 6% range through 2026 (see graph below):

In other words, no big changes are expected. But small shifts, like the one we just saw, are still likely.

What Rate Would Get Buyers Moving Again?

The magic number most buyers seem to be watching for is 6%. And it’s not just a psychological benchmark; it has real impact. A recent report from the National Association of Realtors (NAR) says if rates reach 6%:

And roughly 550,000 people would buy a home within 12 to 18 months

5.5 million more households could afford the median-priced home

That’s a lot of pent-up demand just waiting for the green light. And if you look back at the graph above, you’ll see Fannie Mae thinks we’ll hit that threshold next year. That raises an important question: Does it really make sense to wait for lower rates?

Because here’s the tradeoff. If you’re waiting for 6%, you need to realize a lot of other people are too. And when rates do continue to inch down and more buyers jump into the market all at once, you could face more competition, fewer choices, and higher home prices. NAR explains it like this:

“Home buyers wishing for lower mortgage interest rates may eventually get their wish, but for now, they’ll have to decide whether it’s better to wait or jump into the market.”

Consider the unique window that exists right now:

Inventory is up = more choices

Price growth has slowed down = more realistic pricing

You may have more room to negotiate = you could get a better deal

These are all opportunities that will go away if rates fall and demand surges. That’s why NAR says:

“Buyers who are holding out for lower mortgage rates may be missing a key opening in the market.”

Bottom Line

Some people have told us that they are holding off on making their next move in order to see “what happens.” If that means if rates are going to drop, you have your answer. They aren’t expected to hit 6% this year.

But when rates drop, you’ll have to deal with more competition as other buyers jump back in. If you want less pressure and more negotiating power, that opportunity is already here – and it might not last for long. It all depends on what happens next in the economy.

If you’re thinking about entering the market but want to talk it through, we’re here to listen. You can find us at 508-388-1994 or msennott@todayrealestate.com. Let us know how we can help.

Mari and Hank

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

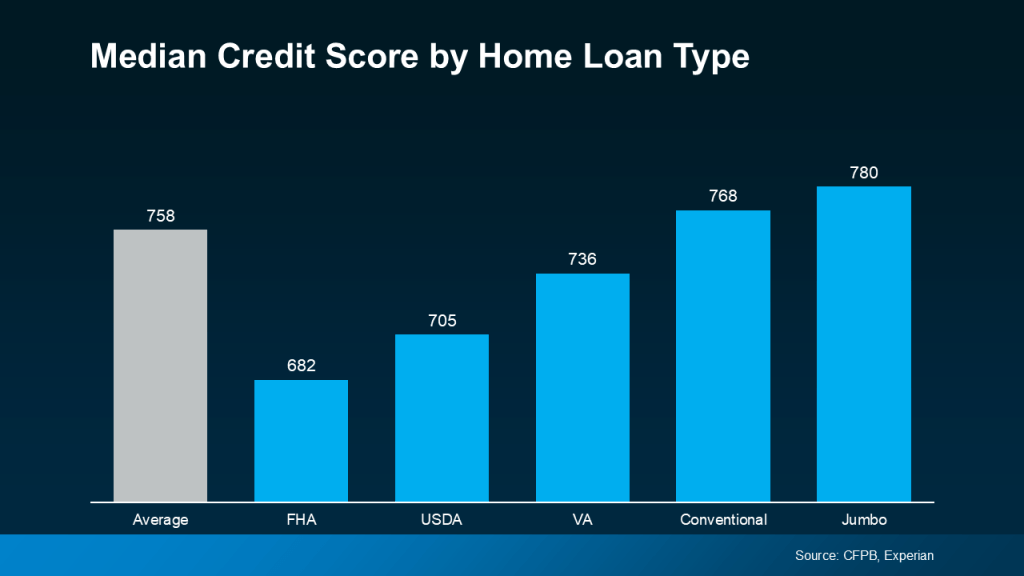

Most homebuyers think they need better credit than they actually do.

According toFannie Mae, 90% of buyers don’t actually know what credit score lenders are looking for, or they overestimate the minimum needed.

Let that sink in. That means most homebuyers think they need better credit than they actually do – and maybe you’re one of them. And that could make you think buying a home is out of reach for you right now, even if that’s not necessarily true. So, let’s look at what the data really says about credit scores and homebuying.

There’s No One Magic Number

There’s no universal credit score you absolutely have to have when buying a home. And that means there’s more flexibility than most people realize. Check out this graph showing the median credit scores recent buyers had among different home loan types:

Here’s what’s important to realize. The numbers vary, and there’s no one-size-fits-all threshold. And that could open doors you thought were closed for you. The best way to learn more is to talk to a trusted lender. As FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

Why Your Score Still Matters

When you buy a home, lenders use your credit score to get a sense of how reliable you are with money. They want to see if you typically make payments on time, pay back debts, and more.

Your score can impact which loan types you may qualify for, the terms on those loans, and even your mortgage rate. And since mortgage rates are a big factor in how much house you’ll be able to afford, that may make your score feel even more important today. As Bankrate says:

“Your credit score is one of the most important factors lenders consider when you apply for a mortgage. Not just to qualify for the loan itself, but for the conditions: Typically, the higher your score, the lower the interest rates and better terms you’ll qualify for.”

That still doesn’t mean your credit has to be perfect. Even if your credit score isn’t as high as you’d like, you may still be able to get a home loan.

Want To Boost Your Score? Start Here

And if you talk to a lender and decide you want to improve your score (and hopefully your loan type and terms too), here are a few smart moves according to the Federal Reserve Board:

Pay Your Bills on Time: This is a big one. Lenders want to see you can reliably pay your bills on time. This includes everything from credit cards to utilities and cell phone bills. Consistent, on-time payments show you’re a responsible borrower.

Pay Down Your Debt: When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible. That makes you a lower-risk borrower in the eyes of lenders – making them more likely to approve a loan with better terms.

Review Your Credit Report: Get copies of your credit report and work to correct any errors you find. This can help improve your score.

Don’t Open New Accounts: While it might be tempting to open more credit cards to build your score, it’s best to hold off. Too many new credit applications can lead to hard inquiries on your report, which can temporarily lower your score.

Bottom Line

Your credit score doesn’t have to be perfect to qualify for a home loan. But a better score can help you get better terms on your home loan. The best way to know where you stand and your options for a mortgage is to connect with a trusted lender.

If you are not working with a reputable lender, we can connect you with several who we know. Just reach out to 508-388-1994 or msennott@todayrealestate.com. We’re happy to help…

Mari and Hank

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

When selling your house, the price you choose isn’t just a number, it’s a strategy.

If you’ve been following the real estate market, you’ve no doubt noticed that there have been a lot of price changes lately. More than we’ve seen in a while.

Does that mean prices are falling? Not exactly. In many cases the seller priced their home too high to begin with.

When selling your house, the price you choose isn’t just a number, it’s a strategy.

The number of homes for sale is climbing. And that means buyers have more choices and can be more selective. If your price doesn’t line up with what else is out there, they’ll go right past it and go on to the next one.

Pricing right from the start is your best move – we can help make sure you do.

Overpricing Comes at a Cost

More sellers are finding that out the hard way. They list their house based on how things were a year ago – or based on a neighbor’s sale that happened under completely different circumstances. Maybe even what they “want.” Then, when their house doesn’t sell, they’re left with three tough choices:

Drop the price: Cutting the price might help get more eyes on the house again, but it can also trigger red flags. Buyers may wonder what’s wrong with it. And that’s going to impact any offers you get after the price cut.

Take it off the market: Some sellers give up on the idea of selling right now. The worst part about this is that it means putting their future plans on the back burner. That dream of more space, downsizing, or relocating? On pause.

Rent it out: Others go the landlord route, but managing tenants and navigating leases isn’t always the simple fallback it seems. Renting can work, but being a landlord is often a lot more hassle than people expect.

None of those options were part of the original plan. And honestly, none of them are where you should end up if you wanted to sell. Here’s a look at how our expertise can help you avoid these headaches. Let’s use price cuts as an example.

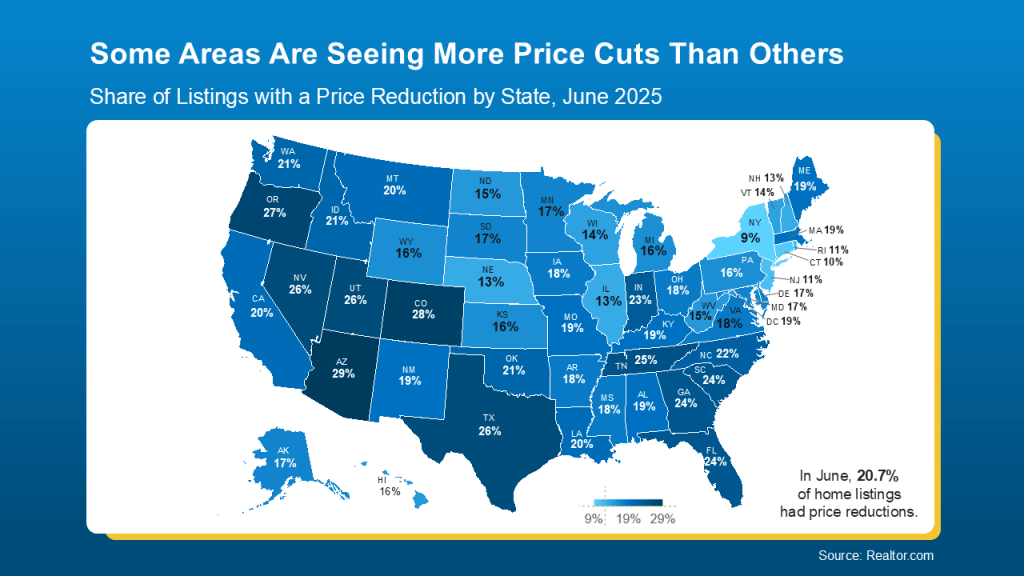

location Makes a Difference

While the number of price cuts is up nationally, this map shows some parts of the country are seeing far more of them than others. It all comes down to how much inventory has grown in that area (see map below):

As Realtor.com explains:

“Regionally, price reductions in June were significantly more common in the South and West (23% of listings) than they were in the Northeast (13% of listings), reflecting the inventory divergence across these regions.”

In Massachusetts, 19% of listings had price reductions.

That means pricing isn’t one-size-fits-all. And that’s why you shouldn’t try to determine your list price on your own.

We can Help You Nail the Price

We just don’t just toss out a number or tell you what you want to hear.

As Zillow says:

“Well-priced homes are more likely to sell quickly, but pricing your home to sell quickly and for maximum dollar requires strategy and knowledge of your local market. You need to have a clear-eyed view of your home in relation to the competition, and knowledge about whether you’re in a buyers or sellers market. It also helps to know what buyers in your area can afford.”

And that’s all knowledge we have. We know the Cape Cod market, compare recent sales, and factor in your goals and buyer behavior. Based on what’s happening, sometimes the best play will be pricing right at current market value. Other times pricing a little lower actually will spark more offers and ultimately get you a better final sale price.

Bottom Line

Overpricing can lead to tough choices you never want to face. But with the right price, and the right guidance, you can skip the stress and sell with confidence. Let’s connect so you have a pricing strategy that works for today’s market and gets you where you want to go. You can always find us at 508-388-1994 or msennott@todayrealestate.com.

Mari and Hank

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

Are you thinking about selling your house? Here are some common mistakes that are being made right now that’s causing the process to be more stressful for some sellers. And even costing them money!

Fortunately, they’re easy to avoid, as long as you know what to watch for. Let’s break down the biggest seller slip-ups, and how we can help you steer clear of them.

1. Overpricing Your House

It’s completely natural to want top dollar for your house, especially if you’ve put a lot of work into it. But in today’s shifting market, pricing it too high can backfire. Investopedia explains:

“Setting a list price too high could mean your home struggles to attract buyers and stays on the market for longer.”

And your house sitting on the market for a long time could lead to price cuts that raise red flags about “what’s wrong” with the property. That’s why pricing your house right from the start matters.

To advise you on price, we look at what other similar nearby homes have sold for, the condition of your house, and what’s happening in the market right now. That way we can suggest a price that’s more likely to bring in buyers, and maybe even more than one offer.

2. Spending Money on the Wrong Upgrades

The housing market has nearly a half million more sellers than buyers according to Redfin. That means you have more competition as a seller and may have to do a bit more to get your house ready to sell. But not all projects are going to be worth it. If you spend money on the wrong projects, it could really cut into your profit.

We work with buyers and know what they’re really looking for, so we can help you figure out which projects are worth it, and which ones to skip. Even better, we know how to highlight any upgrades you make in your home, so your house stands out online and gets more attention.

3. Refusing To Negotiate

Now that inventory has grown, it’s important to stay flexible. Buyers have more options – and with it comes more negotiating power. U.S. News explains:

“If you’ve received an offer for your house that isn’t quite what you’d hoped it would be, expect to negotiate . . . make sure the buyer also feels like he or she benefits . . . consider offering to cover some of the buyer’s closing costs or agree to a credit for a minor repair the inspector found.”

Again, that’s where we come in. We’ll advise you on what’s normal in today’s market, and how to find a win-win solution. Sometimes making a small compromise can keep the deal moving and help you move on to your next chapter faster.

4. Skipping Research When Hiring an Agent

So, you want to interview several agents? Be sure to do your research.

Ask about how many homes has the person sold? (We’ve sold 400.)

Ask about their marketing plan. (We have one.)

Ask about how committed they are to representing your home. (Are they going to attend every showing or just give the lock box code to any agent who calls. We attend every showing. If we’re not there to sell your home, then why did you hire us? If for some reason we can’t, another Today Real Estate agent who is fully briefed about your home will.)

Bottom Line

Selling a house doesn’t have to be stressful, especially if you have us by your side. If you’re ready to sell, let’s talk. You can find us at 508-388-1994 or msennott@todayrealestate.com.

Over the past few years, affordability has been the biggest challenge for many homebuyers. Between home prices and mortgage rates, many have felt stuck between a rock and a hard place.

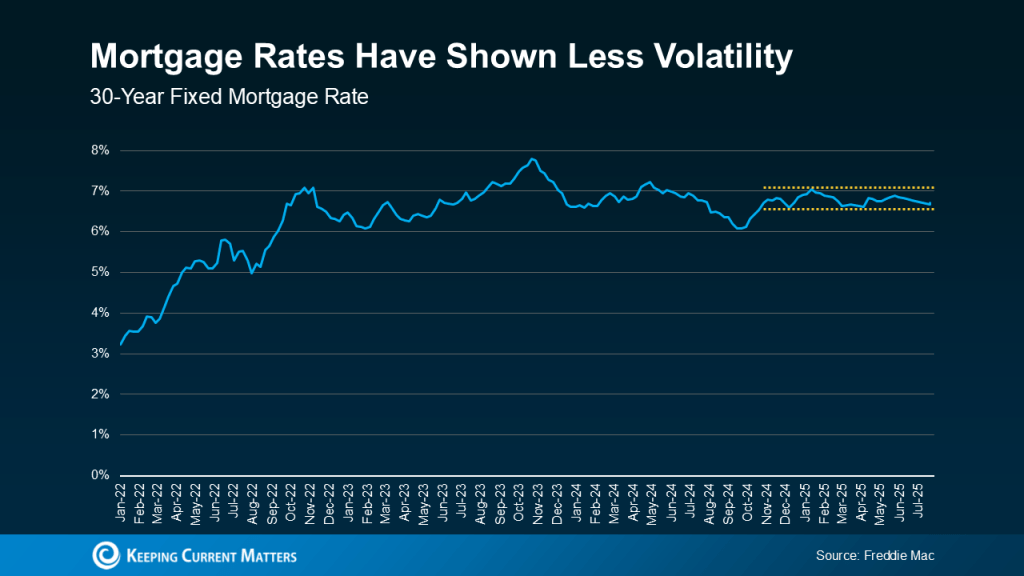

But the situation is getting better. While affordability is still tight, mortgage rates have shown signs of stabilizing in recent months.

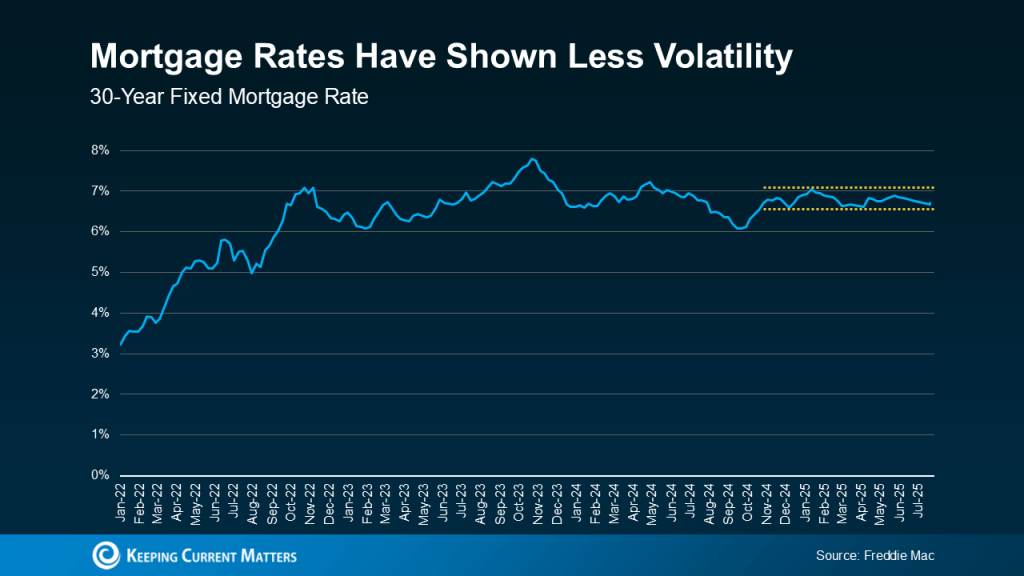

Mortgage Rates Have Stabilized – For Now

Over the past year, mortgage rates have had their share of ups and downs, making it tough for buyers to know what to expect. But recently, rates have started to level out and have settled into a more narrow range (see graph below):

As the graph shows, rates have stayed within that half-percentage-point since late last year. Yes, there’s been movement within that range, but wild swings and sudden ups and downs just haven’t been the story lately. And that’s a bigger deal than you may realize. As HousingWire explains:

“Analysts, economists and mortgage professionals are coining this quarter’s activity as one of the most “calm” periods for mortgage rates in recent memory.”

How This Helps you

Let’s be real. Unpredictability makes it tough to plan ahead. When rates are bouncing around and making big jumps week to week, it’s easy to be intimidated. But with rates staying in a pretty steady range over the past several months, you have a clearer picture of what your potential monthly payment could look like. That makes moving feel less uncertain – and more doable.

So, you can start planning if you’ve decided that it’s time to make a change.Life goes on. Your home that is too small isn’t going to get any bigger. And it’s not going to shrink if it’s already too big.

Will This Stability Last?

According to the experts, it looks like that stability might hang around for a bit. Rates may come down ever so slightly in the months ahead, but it’ll likely be a slow and mild change. As Danielle Hale, Chief Economist at Realtor.com, says:

“I expect a generally downward trend for rates this year, but at a slow enough pace that it might not be noticeable in any given month.”

So, if you’ve been holding out for the perfect mortgage rate, the best advice is to avoid trying to time the market. It may not look terribly different than the opportunity you already have in front of you. As Jeff Ostrowski, Housing Market Analyst at Bankrate, explains:

“Trying to time mortgage rates is really difficult. There’s no guarantee that rates are going to be any more favorable in three months or six months.”

And if we look at the latest expert forecasts that go out a bit further, even those tell much of the same story. Two out of the three projections say rates will still likely be in the mid-6% range by the end of 2026 (see graph below):

This puts today’s buyers in a much better spot. As Sam Khater, Chief Economist at Freddie Mac, explains:

“Mortgage rates have moved within a narrow range for the past few months . . . Rate stability, improving inventory and slower house price growth are an encouraging combination . . .”

Just remember, mortgage rates are still going to react to changing economic conditions, inflation, and more – and that means they could shift again. But right now, you’ve got more predictability, and that means more opportunity, too.

Remember: the rates you see quoted may not be the rate you could get. For example, Cape Cod Five is showing rates as low as 5.625% for a 15-year fixed rate mortgage. Your individual situation determines your rate.

Bottom Line

So, if you haven’t spoken with your mortgage lender in a while you might want to give him or her a call.

If you don’t have a relationship with a lender, we can recommend several whom we’ve worked with. You can find us at 508-388-1994 or msennott@todayrealestate.com. We’re happy to help…

Mari and Hank

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

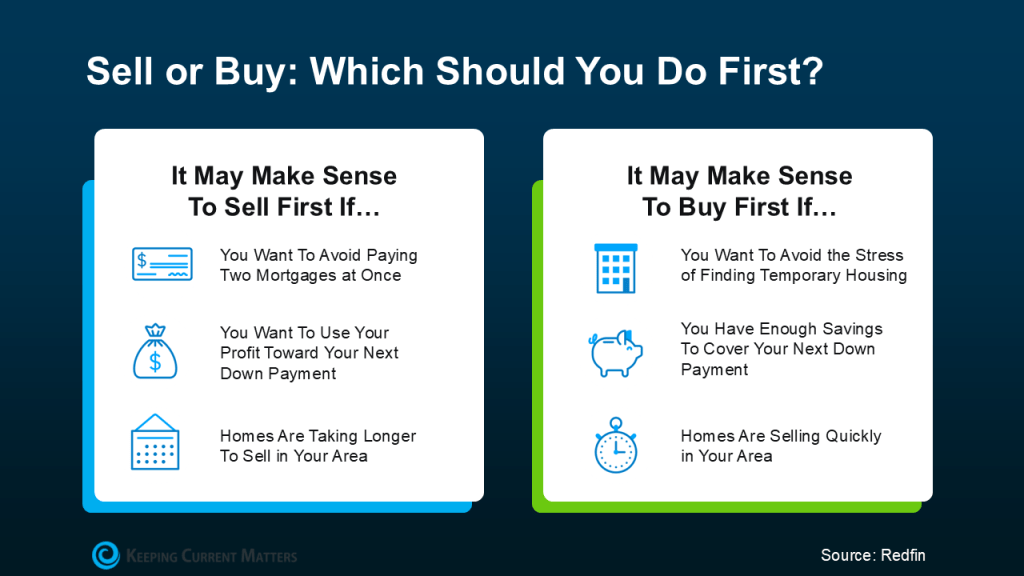

If you’re a homeowner planning to move, you’re probably wondering what the process is going to look like and which you should tackle first:

Is it better to start by finding your next home?

Or should you sell your current house before you go out looking?

Ultimately, what’s right for you depends on a lot of factors.And that’s where we can really help make your next step clear.

We know the market, the latest trends, and what’s working for other homeowners right now. We can make a recommendation based on our expertise and your needs.

But here’s a little bit of a sneak peek. In many cases today, getting your current home on the market first can put you in a better spot. Here’s why that order tends to work best.

The Advantages of Selling First

1. You’ll Unlock Your Home Equity

Selling your current home before you try to buy your next one allows you to access the equity you’ve built up – and based on home price appreciation over the past few years, that’s no small number. Data from Cotality (former CoreLogic) shows that the average homeowners is sitting on $302K in equity today.

And once you sell, you can use that equity to pay for the down payment on your next house (and maybe even more). You could even have enough to buy your next house in cash. That’s a big deal, and it could make your next move a whole lot easier on your wallet.

There are also ways to use the equity in your home before selling that we can discuss. (That’s how we bought our home three years ago when we downsized.)

2. You Won’t Be Juggling Two Mortgages

Trying to buy before you sell means you could wind up holding two mortgages, even if just for a few months. That can get expensive, fast – especially if there are unexpected repairs or delays. Selling first removes that stress and helps you move forward without the financial strain. As Ramsey Solutions says: “It’s best to sell your old home before buying a new one to avoid unnecessary risks and possible headaches.”

3. You’ll Be in a Stronger Position When You Make an Offer

Sellers love a clean, simple offer. If you’ve already sold your house, you don’t need to make your offer contingent on that sale – and that can help you stand out. We can position your offer as strong, so you have the best shot at getting the home you want.

This can be a big advantage in competitive markets where sellers prefer buyers with fewer strings attached.

One Thing To Keep in Mind

But like with anything in life, there are tradeoffs. As you weigh your options, consider this potential drawback, too:

1. You May Need a Place To Stay (Temporarily)

Once your house sells, you may need a short-term rental or to stay with family until you can move into your next home. We can help you negotiate things like a post-closing occupancy (renting the home from the buyer for a set period) or flexible closing dates to help smooth out that transition as much as possible.

Here’s a simple visual that can help you think through your options (see below):

Bottom Line

In many cases, selling first doesn’t just give you clarity, it gives you options. It helps you buy with more confidence, more financial power, and less pressure.

If you’re ready to make a move but not sure where to begin, let’s talk. We will walk you through your equity, your timing, and what’s going on in the market right now so you can decide what’s right for you.

You can find us at 508-388-1994 or msennott@todayrealestate.com.

Mari and Hank

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

Maybe you’ve seen headlines saying home sales are down compared to last year. You might even be thinking – is it even a good time to sell?

Here’s the thing. There’s no denying that the pace of the market has cooled compared to the frenzy we saw just a few years ago. Cumulative days on market for 2025 is 61 as opposed to 47 one year ago. But that’s not a red flag. It’s a return to normal. And normal doesn’t mean nothing’s happening. Buyers are still out there – and homes are still selling.

Why? Because real life doesn’t pause for perfect conditions. There are always people who need to buy – and this year is no exception. Buyers who are in the middle of a big change in their lives, a new marriage, a growing family, or a new job still need to move, no matter where mortgage rates are. And they may be looking for a home just like yours.

Every Minute 8 Homes Sell

Let’s break it down using the latest sales from the National Association of Realtors (NAR). Based on the current pace, we’re on track to sell 4.03 million homes this year (not including new construction).

4.03 million homes ÷ 365 days = 11,041 homes sell per day

11,041 homes ÷ 24 hours = 460 homes sell per hour

460 homes ÷ 60 minutes = roughly 8 homes sell every minute

That means in the time it takes to read this; another 8 homes will sell. Let that sink in. Every minute, buyers are making moves – and sellers are closing deals.

If you’ve been holding off on selling your house because you think buyers aren’t out there, let this reassure you – there are still buyers looking to buy.

On Cape Cod more than 900 single family homes have closed this year with nearly 1,100 more pending. The median sales price for the year thus far is $756,490.00. That’s 3% higher than last year.

Remember: median sales price is the midway point. There are just as many homes for sales below the median price as above.

But since the market is balancing out, selling today takes more than just putting up a sign in the yard. You’ve got to price your house right, market it well, and know how to reach the buyers who are ready to act. That’s where we come in.

We’ll help you navigate this market, position your home to stand out, and guide you through every step.

We know the market so we also can assist you in finding the right home that meets your goals.

Bottom Line

The market hasn’t stopped. Buyers are still buying. Life is still happening. And if selling your home or buying one (or both!) is part of your next chapter, you can make it happen.

Roughly 11,000 homes are selling every day. When you’re ready to make the change you need to, let’s connect at 508-388-1994 or msennott@todayrealestate.com and we’ll start working on where’s next for you.

Mari and Hank

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.

Are you thinking about buying a home, but not sure if this is the right time? A lot of people are waiting and wondering what the market’s going to do next. But here’s something only the savviest buyers realize:

This summer might actually be the best time to buy in years. Here are three big reasons why.

1. You Have More Negotiating Power

After several years of sellers having all the leverage, things are starting to shift. Check out the graph below. It uses data from Redfin to show that right now, there are more sellers active in the market than buyers:

Take a look at what happened back in 2021 through roughly 2023. In that time period, there were far more buyers (the blue line) looking to buy than homes for sale (the green line). That’s what drove the intense competition, bidding wars, and the exponential price growth the market saw back then.

Now, the market has shifted, and buyers are regaining their negotiating power as a result. With more sellers than buyers, sellers may be more willing to pay for repairs, cover some of your closing costs, or lower their asking price. The return of this kind of normal balance is a sign of a much healthier, more sustainable market. As Lawrence Yun, Chief Economist of the National Association of Realtors (NAR), explains:

“ . . . with housing inventory levels reaching five-year highs, homebuyers in nearly every region of the country are in a better position to negotiate more favorable terms.”

And just in case you’re worried there are too many homes on the market, here’s what you should know. Overall inventory is still lower than normal, so you don’t have to worry about a nationwide oversupply or a crash.

As we noted in our post last week, inventory has increased on Cape Cod, as well. But it is still not close to pre-pandemic levels. So, if you’re waiting for that crash that your Uncle Bob who “knows a little something about real estate” is talking about, you’re going to have a long wait.

2. You Have More Choices

The number of homes for sale has improved a lot. Based on the latest data from Realtor.com, more homes were listed this May than in May 2024 or May 2023 (see graph below):

And more homes for sale means more choices. There’s a good chance your perfect match just hit the market – or it will soon. So, it’s a great time to explore what’s out there. As Jake Krimmel, Economist at Realtor.com, says:

“With more fresh inventory hitting the market, buyers have better opportunities to find a home that fits their needs.”

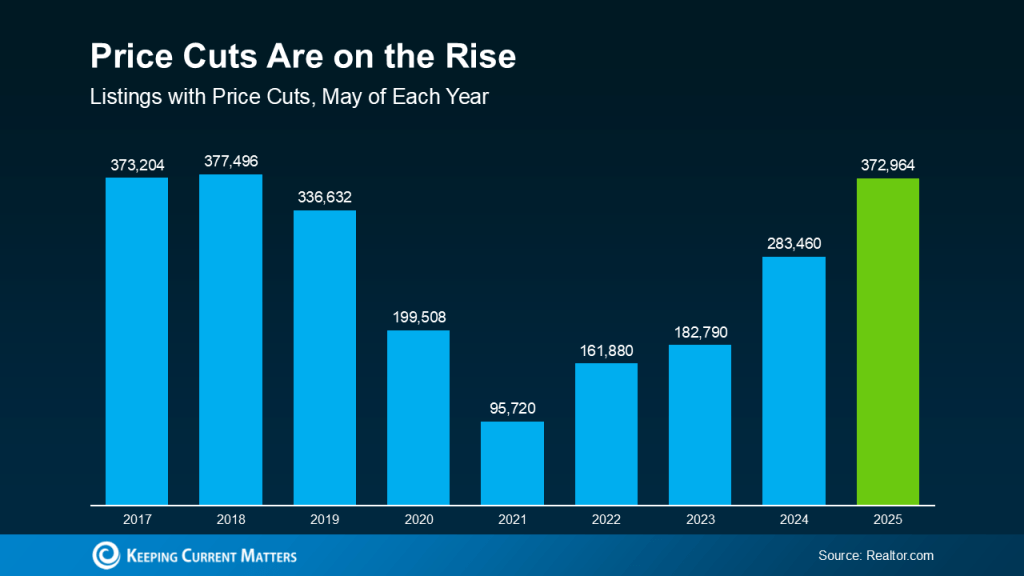

3. You May See More Flexibility on Price

With more homes for sale, they’re not selling at the same frenzied pace they were just a few years ago.

Since homes are taking more time to sell, some sellers are choosing to lower their asking prices to draw buyers back in or speed up the process. And that’s to-be-expected. According to Realtor.com, 19.1% of listings had a price cut this May (see graph below):

That’s the fifth straight month where more sellers have reduced their price. And, as of May, the volume of price cuts is back at normal levels. This is yet another sign of the return to a more balanced market.

While you shouldn’t expect a big discount, you may find sellers are a bit more flexible right now. As a recent article from The Street says:

“Although sellers have had the upper hand in the housing market over the past few years, houses are now staying on the market for longer, shifting negotiating power back to homebuyers.”

Just remember, most sellers still aren’t adjusting their prices – just the ones who overpriced to start with. So, this isn’t a sign of a crash, it’s a sign of some sellers having outdated expectations in a shifting market.

Bottom Line

This summer brings a powerful combo for buyers: more homes to choose from, less competition, and sellers being more flexible on pricing.

What would finding the right home this summer mean for your next chapter? If you’re ready to find out, let’s connect at 508-360-5664 or msennott@todayrealestate.com.

Selling your house without an agent as a “For Sale by Owner” (FSBO) may be something you’ve considered. Everyone knows someone who knows someone who sold a home on their own and everything went “just fine.”

But did it really?

Did they leave money on the table? Agree to a concession that they didn’t need to? Spend too much on legal fees? When it was all over, how much money did they really save by not hiring a real estate professional to manage the sale??

You don’t hear much about any of that because maybe the “successful” seller doesn’t understand what they lost.

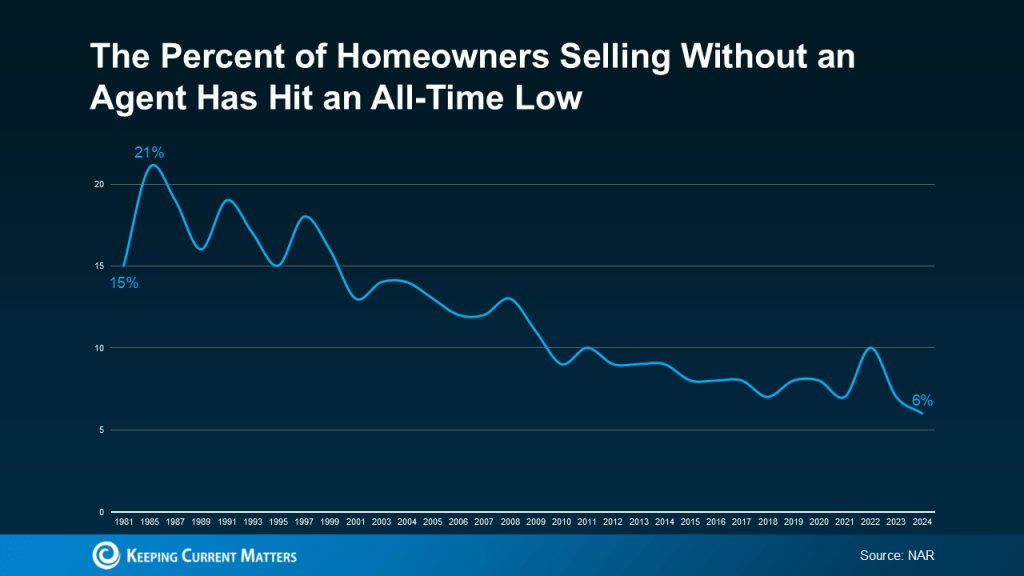

Here’s what you need to know. In today’s shifting market, more homeowners are deciding that it’s not worth the risk to go it alone.

According to the latest data from the National Association of Realtors (NAR), the number of homeowners selling without professional assistance has hit an all-time low (see graph below):

And for the small number of homeowners who do decide to sell on their own, data shows they’re still not confident they’re making a good choice.

A recent survey finds three out of every four homeowners who don’t plan to use an agent have doubts about whether that’s actually the right decision.

And here’s why. The market is changing – not in a bad way, just in a way that requires a smarter, more strategic approach. And having a professional in your corner really pays off.

Here are just two of the ways our expertise makes a difference.

1. Getting the Price Right in a Market That’s Evolving

One of the biggest hurdles when selling a house on your own is figuring out the right price. It’s not as simple as picking a price that you want, sounds good, or is what your neighbor’s home sold for a few years back – you need to hit the bullseye for where the market is right now. Without professional to help, you’re more likely to miss. As Zillow explains:

“Agents are pros when it comes to pricing properties and have their finger on the pulse of your local market. They understand current buying trends and can provide insight into how your home compares to others for sale nearby.”

Basically, we know what’s really selling, what buyers are willing to pay today, and how to position your house to sell quickly. That kind of insight can have a big impact, especially in a market that’s balancing out.

2. Handling (and Actually Understanding) the Legal Documents

There’s also a mountain of documentation when selling a house, including everything from disclosures to seller and buyer contracts. A mistake can have big legal implications. This is another area where we can help.

We’ve handled these documents countless times and know exactly what’s needed to keep everything on track, so you avoid delays. And now that buyers are including more contingencies and asking for concessions again, we can guide you step by step, making sure everything is done right and documented correctly the first time.

Selling Your House Quickly in a Shifting Market

Even though inventory has grown, homes aren’t selling at quite the same pace as they were. But you can still sell quickly if you have a proven plan to help your house stand out.

Just remember, as a homeowner you don’t have the same network or marketing tools that we do. Selling a house is more than sticking a sign in the ground and putting a posting on Facebook.

We’ve sold over 400 homes.

So, if you want the process to happen in a timely manner, let’s connect at 508-388-1994 or msennott@todayrealestate.com.