If you’ve been following the real estate market, you’ve no doubt noticed that there have been a lot of price changes lately. More than we’ve seen in a while.

Does that mean prices are falling? Not exactly. In many cases the seller priced their home too high to begin with.

When selling your house, the price you choose isn’t just a number, it’s a strategy.

The number of homes for sale is climbing. And that means buyers have more choices and can be more selective. If your price doesn’t line up with what else is out there, they’ll go right past it and go on to the next one.

Pricing right from the start is your best move – we can help make sure you do.

Overpricing Comes at a Cost

More sellers are finding that out the hard way. They list their house based on how things were a year ago – or based on a neighbor’s sale that happened under completely different circumstances. Maybe even what they “want.” Then, when their house doesn’t sell, they’re left with three tough choices:

- Drop the price: Cutting the price might help get more eyes on the house again, but it can also trigger red flags. Buyers may wonder what’s wrong with it. And that’s going to impact any offers you get after the price cut.

- Take it off the market: Some sellers give up on the idea of selling right now. The worst part about this is that it means putting their future plans on the back burner. That dream of more space, downsizing, or relocating? On pause.

- Rent it out: Others go the landlord route, but managing tenants and navigating leases isn’t always the simple fallback it seems. Renting can work, but being a landlord is often a lot more hassle than people expect.

None of those options were part of the original plan. And honestly, none of them are where you should end up if you wanted to sell. Here’s a look at how our expertise can help you avoid these headaches. Let’s use price cuts as an example.

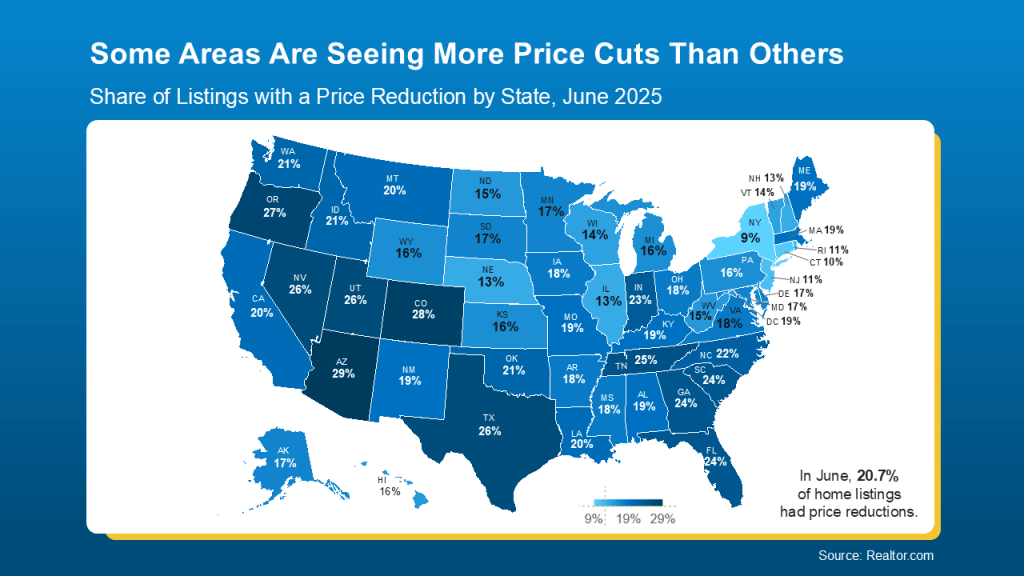

location Makes a Difference

While the number of price cuts is up nationally, this map shows some parts of the country are seeing far more of them than others. It all comes down to how much inventory has grown in that area (see map below):

“Regionally, price reductions in June were significantly more common in the South and West (23% of listings) than they were in the Northeast (13% of listings), reflecting the inventory divergence across these regions.”

In Massachusetts, 19% of listings had price reductions.

That means pricing isn’t one-size-fits-all. And that’s why you shouldn’t try to determine your list price on your own.

We can Help You Nail the Price

We just don’t just toss out a number or tell you what you want to hear.

As Zillow says:

“Well-priced homes are more likely to sell quickly, but pricing your home to sell quickly and for maximum dollar requires strategy and knowledge of your local market. You need to have a clear-eyed view of your home in relation to the competition, and knowledge about whether you’re in a buyers or sellers market. It also helps to know what buyers in your area can afford.”

And that’s all knowledge we have. We know the Cape Cod market, compare recent sales, and factor in your goals and buyer behavior. Based on what’s happening, sometimes the best play will be pricing right at current market value. Other times pricing a little lower actually will spark more offers and ultimately get you a better final sale price.

Bottom Line

Overpricing can lead to tough choices you never want to face. But with the right price, and the right guidance, you can skip the stress and sell with confidence. Let’s connect so you have a pricing strategy that works for today’s market and gets you where you want to go. You can always find us at 508-388-1994 or msennott@todayrealestate.com.

Mari and Hank

Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision.